A 1031 exchange is a powerful tool that can help investors defer taxes when they sell one investment property and buy another. However, there are some common mistakes that investors make during the process that can cost them time and money. In this article, we will discuss some of the most common mistakes to avoid in a 1031 exchange.

Mistake #1: Not understanding the 1031 Exchange timeline

The IRS has specific rules and timelines that must be followed in a 1031 exchange. Investors have 45 days from the sale of their relinquished property to identify potential replacement properties and 180 days to complete the purchase of one or more of those identified replacement properties. Failure to meet these deadlines will result in the disqualification of the 1031 exchange, meaning that the investor will be responsible for paying taxes on any capital gains realized from the sale of the relinquished property.

Mistake #2: Not using a 1031 Exchange Qualified Intermediary

A Qualified Intermediary (QI) is a third-party facilitator that through a series of assignments acts as the party to complete the exchange with the Exchanger. By virtue of these assignments, title to the Relinquished Party passes through the QI to the Buyer, and title to the Replacement Property passes through the QI to the Exchanger. Title does not actually vest in the QI, saving a legal step, and in many states, additional transfer taxes. The QI ensures a valid 1031 exchange by properly structuring the exchange per IRC 1031, preparing all necessary exchange documents, and monitoring the exchange to ensure continued compliance throughout the process. Failure to use a QI can result in missteps causing the disqualification of the exchange and the loss of tax deferral benefits.

Mistake #3: Not properly identifying replacement property

Investors must follow strict identification rules when selecting replacement properties in a 1031 exchange. They must identify potential replacement properties within 45 days of the sale of their relinquished property, and they must follow one of three identification rules: the Three-Property Rule, the 200% Rule, or the 95% Rule. (These rules are discussed in more detail here: [insert blog link]) Failure to properly identify replacement properties can result in the disqualification of the exchange.

Mistake #4: Mixing personal and business property

A 1031 exchange is only applicable to investment or business property. It cannot be used for personal property, such as a primary residence. Mixing personal and business property can result in the disqualification of the exchange, unless great care is exercised in structuring the exchange.

Mistake #5: Not consulting with a tax professional

The rules and regulations surrounding a 1031 exchange can be complex and confusing. It is important to consult with a tax professional who is familiar with the intricacies of the process to ensure that all requirements are met and mistakes are avoided. Failure to consult with a tax professional can result in costly errors and the loss of tax deferral benefits.

In conclusion, a 1031 exchange can be an effective way to defer taxes on investment properties. However, it is important to understand the rules and requirements of the process in order to avoid common mistakes that will result in the disqualification of the exchange. By working with a Qualified Intermediary and consulting with a tax professional, investors can ensure a successful 1031 exchange and maximize their tax deferral benefits.

Category: 1031 Exchange General

-

Common Mistakes to Avoid in a 1031 Exchange

-

Common Mistakes to Avoid in a 1031 Exchange

A 1031 exchange is a powerful tool that can help investors defer taxes when they sell one investment property and buy another. However, there are some common mistakes that investors make during the process that can cost them time and money. In this article, we will discuss some of the most common mistakes to avoid in a 1031 exchange.

Mistake #1: Not understanding the 1031 Exchange timeline

The IRS has specific rules and timelines that must be followed in a 1031 exchange. Investors have 45 days from the sale of their relinquished property to identify potential replacement properties and 180 days to complete the purchase of one or more of those identified replacement properties. Failure to meet these deadlines will result in the disqualification of the 1031 exchange, meaning that the investor will be responsible for paying taxes on any capital gains realized from the sale of the relinquished property.

Mistake #2: Not using a 1031 Exchange Qualified Intermediary

A Qualified Intermediary (QI) is a third-party facilitator that through a series of assignments acts as the party to complete the exchange with the Exchanger. By virtue of these assignments, title to the Relinquished Party passes through the QI to the Buyer, and title to the Replacement Property passes through the QI to the Exchanger. Title does not actually vest in the QI, saving a legal step, and in many states, additional transfer taxes. The QI ensures a valid 1031 exchange by properly structuring the exchange per IRC 1031, preparing all necessary exchange documents, and monitoring the exchange to ensure continued compliance throughout the process. Failure to use a QI can result in missteps causing the disqualification of the exchange and the loss of tax deferral benefits.

Mistake #3: Not properly identifying replacement property

Investors must follow strict identification rules when selecting replacement properties in a 1031 exchange. They must identify potential replacement properties within 45 days of the sale of their relinquished property, and they must follow one of three identification rules: the Three-Property Rule, the 200% Rule, or the 95% Rule. (These rules are discussed in more detail here: [insert blog link]) Failure to properly identify replacement properties can result in the disqualification of the exchange.

Mistake #4: Mixing personal and business property

A 1031 exchange is only applicable to investment or business property. It cannot be used for personal property, such as a primary residence. Mixing personal and business property can result in the disqualification of the exchange, unless great care is exercised in structuring the exchange.

Mistake #5: Not consulting with a tax professional

The rules and regulations surrounding a 1031 exchange can be complex and confusing. It is important to consult with a tax professional who is familiar with the intricacies of the process to ensure that all requirements are met and mistakes are avoided. Failure to consult with a tax professional can result in costly errors and the loss of tax deferral benefits.

In conclusion, a 1031 exchange can be an effective way to defer taxes on investment properties. However, it is important to understand the rules and requirements of the process in order to avoid common mistakes that will result in the disqualification of the exchange. By working with a Qualified Intermediary and consulting with a tax professional, investors can ensure a successful 1031 exchange and maximize their tax deferral benefits. -

Common Mistakes to Avoid in a 1031 Exchange

A 1031 exchange is a powerful tool that can help investors defer taxes when they sell one investment property and buy another. However, there are some common mistakes that investors make during the process that can cost them time and money. In this article, we will discuss some of the most common mistakes to avoid in a 1031 exchange.

Mistake #1: Not understanding the 1031 Exchange timeline

The IRS has specific rules and timelines that must be followed in a 1031 exchange. Investors have 45 days from the sale of their relinquished property to identify potential replacement properties and 180 days to complete the purchase of one or more of those identified replacement properties. Failure to meet these deadlines will result in the disqualification of the 1031 exchange, meaning that the investor will be responsible for paying taxes on any capital gains realized from the sale of the relinquished property.

Mistake #2: Not using a 1031 Exchange Qualified Intermediary

A Qualified Intermediary (QI) is a third-party facilitator that through a series of assignments acts as the party to complete the exchange with the Exchanger. By virtue of these assignments, title to the Relinquished Party passes through the QI to the Buyer, and title to the Replacement Property passes through the QI to the Exchanger. Title does not actually vest in the QI, saving a legal step, and in many states, additional transfer taxes. The QI ensures a valid 1031 exchange by properly structuring the exchange per IRC 1031, preparing all necessary exchange documents, and monitoring the exchange to ensure continued compliance throughout the process. Failure to use a QI can result in missteps causing the disqualification of the exchange and the loss of tax deferral benefits.

Mistake #3: Not properly identifying replacement property

Investors must follow strict identification rules when selecting replacement properties in a 1031 exchange. They must identify potential replacement properties within 45 days of the sale of their relinquished property, and they must follow one of three identification rules: the Three-Property Rule, the 200% Rule, or the 95% Rule. (These rules are discussed in more detail here: [insert blog link]) Failure to properly identify replacement properties can result in the disqualification of the exchange.

Mistake #4: Mixing personal and business property

A 1031 exchange is only applicable to investment or business property. It cannot be used for personal property, such as a primary residence. Mixing personal and business property can result in the disqualification of the exchange, unless great care is exercised in structuring the exchange.

Mistake #5: Not consulting with a tax professional

The rules and regulations surrounding a 1031 exchange can be complex and confusing. It is important to consult with a tax professional who is familiar with the intricacies of the process to ensure that all requirements are met and mistakes are avoided. Failure to consult with a tax professional can result in costly errors and the loss of tax deferral benefits.

In conclusion, a 1031 exchange can be an effective way to defer taxes on investment properties. However, it is important to understand the rules and requirements of the process in order to avoid common mistakes that will result in the disqualification of the exchange. By working with a Qualified Intermediary and consulting with a tax professional, investors can ensure a successful 1031 exchange and maximize their tax deferral benefits. -

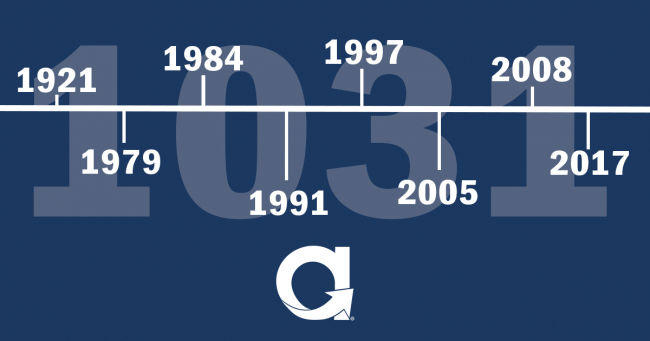

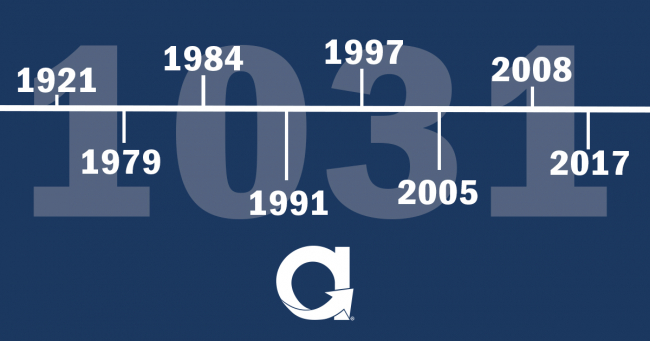

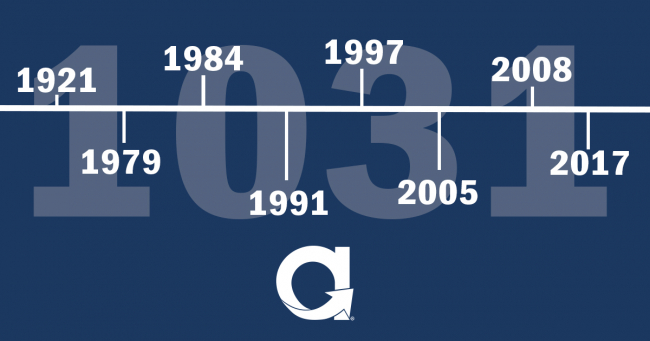

How the 1031 Exchange Process has Evolved Over Time

The 1031 Exchange has been a popular tax strategy for real estate investors for over a century, but its history and evolution are often overlooked. By understanding how this tax strategy has developed and changed over time, investors can make more informed decisions about their investments and take advantage of the benefits associated with a 1031 Exchange.

Originally established as part of the Revenue Act of 1921, 1031 Exchanges were designed to encourage investment and growth in the real estate market. The basic idea behind the exchanges was simple; by allowing investors to exchange one property for another without incurring capital gains, or other related taxes, the government could incentivize investors to keep their money in real estate and continue investing in new properties.

Over the years, the rules and regulations governing 1031 Exchanges have changed in response to new economic and political realities. For example, in 1979, the 9th US Circuit Court of Appeals approved “delayed exchanges” in the Starker case, which allowed investors to sell their property before acquiring a replacement property, therefore eliminated the requirement for a simultaneous exchange. The case involved not only the first non-simultaneously structured exchange but provided for a five-year time frame for Starker to receive his replacement property. In direct response to the open-ended period, in 1984, Congress codified the 45 and 180-day restrictions presented in Starker {Sec. 1031(a)(3)}, and prohibited exchanges of partnership interests {Sec. 1031(a)(2)(D)}. These narrower time frames provided a nexus between the sale and purchase.

In 1991, Section 1031 Regulations were issued, outlining four “Safe Harbors” including: how the exchange funds could be held so that the Taxpayer was not in constructive receipt; allowing funds to be put into a Trust or Escrow; the use of a Qualified Intermediary which took the place of the buyer in connection with the Taxpayers intent to exchange and; allowing the Taxpayer to earn interest on their funds, which previously was not allowed because that would be considered in “constructive receipt” of the funds.

In 1997, the Taxpayer Relief Act introduced a provision stating that domestic property and foreign property are not considered like-kind. This means that real estate investors could no longer exchange their domestic properties for foreign ones or vice versa using a 1031 exchange. However, the act did not change the rules around like-kind exchanges for properties within the United States. This clarification helped to ensure that investors could continue to use 1031 exchanges as a powerful tax strategy for domestic real estate investments. It also remained possible to exchange one foreign property for another foreign property.

In 2005, the IRS issued Revenue Procedure 2005-14, which provided guidance for combining Section 121 and Section 1031, which has implications for (a) rental property converted to primary residence, and (b) primary residence converted to rental property.

In 2008, the IRS issued Revenue Procedure 2008-16 which provided addition guidance and restrictions on vacation/second homes. The restrictions included the requirement that the Relinquished Property be held for investment for at least 24 months immediately preceding the exchange, and within each of the 12-months the property must have been rented out at fair market value for at least 14 days, and the owners personal use could not exceed 14 days or 10% of the total time the property was rented out. The same restrictions were put place for the Replacement Property.

More recently, the Tax Cuts and Jobs Act of 2017 made significant changes to the 1031 Exchange process, eliminating the ability to use 1031 Exchanges for personal property and limiting its use to real estate investments. The act also introduced new restrictions on the types of properties that could be exchanged, including stricter requirements for vacation homes and other non-primary residences.

Despite these changes, the core idea behind the 1031 exchange process remains the same, to incentivize real estate investment and promote growth in the real estate market. Whether you’re a seasoned investor or just getting started in the world of real estate, understanding the history and evolution of 1031 Exchanges is essential to making informed decisions about your investments and maximizing the benefits of this powerful tax strategy. -

How the 1031 Exchange Process has Evolved Over Time

The 1031 Exchange has been a popular tax strategy for real estate investors for over a century, but its history and evolution are often overlooked. By understanding how this tax strategy has developed and changed over time, investors can make more informed decisions about their investments and take advantage of the benefits associated with a 1031 Exchange.

Originally established as part of the Revenue Act of 1921, 1031 Exchanges were designed to encourage investment and growth in the real estate market. The basic idea behind the exchanges was simple; by allowing investors to exchange one property for another without incurring capital gains, or other related taxes, the government could incentivize investors to keep their money in real estate and continue investing in new properties.

Over the years, the rules and regulations governing 1031 Exchanges have changed in response to new economic and political realities. For example, in 1979, the 9th US Circuit Court of Appeals approved “delayed exchanges” in the Starker case, which allowed investors to sell their property before acquiring a replacement property, therefore eliminated the requirement for a simultaneous exchange. The case involved not only the first non-simultaneously structured exchange but provided for a five-year time frame for Starker to receive his replacement property. In direct response to the open-ended period, in 1984, Congress codified the 45 and 180-day restrictions presented in Starker {Sec. 1031(a)(3)}, and prohibited exchanges of partnership interests {Sec. 1031(a)(2)(D)}. These narrower time frames provided a nexus between the sale and purchase.

In 1991, Section 1031 Regulations were issued, outlining four “Safe Harbors” including: how the exchange funds could be held so that the Taxpayer was not in constructive receipt; allowing funds to be put into a Trust or Escrow; the use of a Qualified Intermediary which took the place of the buyer in connection with the Taxpayers intent to exchange and; allowing the Taxpayer to earn interest on their funds, which previously was not allowed because that would be considered in “constructive receipt” of the funds.

In 1997, the Taxpayer Relief Act introduced a provision stating that domestic property and foreign property are not considered like-kind. This means that real estate investors could no longer exchange their domestic properties for foreign ones or vice versa using a 1031 exchange. However, the act did not change the rules around like-kind exchanges for properties within the United States. This clarification helped to ensure that investors could continue to use 1031 exchanges as a powerful tax strategy for domestic real estate investments. It also remained possible to exchange one foreign property for another foreign property.

In 2005, the IRS issued Revenue Procedure 2005-14, which provided guidance for combining Section 121 and Section 1031, which has implications for (a) rental property converted to primary residence, and (b) primary residence converted to rental property.

In 2008, the IRS issued Revenue Procedure 2008-16 which provided addition guidance and restrictions on vacation/second homes. The restrictions included the requirement that the Relinquished Property be held for investment for at least 24 months immediately preceding the exchange, and within each of the 12-months the property must have been rented out at fair market value for at least 14 days, and the owners personal use could not exceed 14 days or 10% of the total time the property was rented out. The same restrictions were put place for the Replacement Property.

More recently, the Tax Cuts and Jobs Act of 2017 made significant changes to the 1031 Exchange process, eliminating the ability to use 1031 Exchanges for personal property and limiting its use to real estate investments. The act also introduced new restrictions on the types of properties that could be exchanged, including stricter requirements for vacation homes and other non-primary residences.

Despite these changes, the core idea behind the 1031 exchange process remains the same, to incentivize real estate investment and promote growth in the real estate market. Whether you’re a seasoned investor or just getting started in the world of real estate, understanding the history and evolution of 1031 Exchanges is essential to making informed decisions about your investments and maximizing the benefits of this powerful tax strategy. -

How the 1031 Exchange Process has Evolved Over Time

The 1031 Exchange has been a popular tax strategy for real estate investors for over a century, but its history and evolution are often overlooked. By understanding how this tax strategy has developed and changed over time, investors can make more informed decisions about their investments and take advantage of the benefits associated with a 1031 Exchange.

Originally established as part of the Revenue Act of 1921, 1031 Exchanges were designed to encourage investment and growth in the real estate market. The basic idea behind the exchanges was simple; by allowing investors to exchange one property for another without incurring capital gains, or other related taxes, the government could incentivize investors to keep their money in real estate and continue investing in new properties.

Over the years, the rules and regulations governing 1031 Exchanges have changed in response to new economic and political realities. For example, in 1979, the 9th US Circuit Court of Appeals approved “delayed exchanges” in the Starker case, which allowed investors to sell their property before acquiring a replacement property, therefore eliminated the requirement for a simultaneous exchange. The case involved not only the first non-simultaneously structured exchange but provided for a five-year time frame for Starker to receive his replacement property. In direct response to the open-ended period, in 1984, Congress codified the 45 and 180-day restrictions presented in Starker {Sec. 1031(a)(3)}, and prohibited exchanges of partnership interests {Sec. 1031(a)(2)(D)}. These narrower time frames provided a nexus between the sale and purchase.

In 1991, Section 1031 Regulations were issued, outlining four “Safe Harbors” including: how the exchange funds could be held so that the Taxpayer was not in constructive receipt; allowing funds to be put into a Trust or Escrow; the use of a Qualified Intermediary which took the place of the buyer in connection with the Taxpayers intent to exchange and; allowing the Taxpayer to earn interest on their funds, which previously was not allowed because that would be considered in “constructive receipt” of the funds.

In 1997, the Taxpayer Relief Act introduced a provision stating that domestic property and foreign property are not considered like-kind. This means that real estate investors could no longer exchange their domestic properties for foreign ones or vice versa using a 1031 exchange. However, the act did not change the rules around like-kind exchanges for properties within the United States. This clarification helped to ensure that investors could continue to use 1031 exchanges as a powerful tax strategy for domestic real estate investments. It also remained possible to exchange one foreign property for another foreign property.

In 2005, the IRS issued Revenue Procedure 2005-14, which provided guidance for combining Section 121 and Section 1031, which has implications for (a) rental property converted to primary residence, and (b) primary residence converted to rental property.

In 2008, the IRS issued Revenue Procedure 2008-16 which provided addition guidance and restrictions on vacation/second homes. The restrictions included the requirement that the Relinquished Property be held for investment for at least 24 months immediately preceding the exchange, and within each of the 12-months the property must have been rented out at fair market value for at least 14 days, and the owners personal use could not exceed 14 days or 10% of the total time the property was rented out. The same restrictions were put place for the Replacement Property.

More recently, the Tax Cuts and Jobs Act of 2017 made significant changes to the 1031 Exchange process, eliminating the ability to use 1031 Exchanges for personal property and limiting its use to real estate investments. The act also introduced new restrictions on the types of properties that could be exchanged, including stricter requirements for vacation homes and other non-primary residences.

Despite these changes, the core idea behind the 1031 exchange process remains the same, to incentivize real estate investment and promote growth in the real estate market. Whether you’re a seasoned investor or just getting started in the world of real estate, understanding the history and evolution of 1031 Exchanges is essential to making informed decisions about your investments and maximizing the benefits of this powerful tax strategy. -

10 Key Questions to Ask Before Starting a 1031 Exchange

If you are looking to sell real property that was held for investment or business use, you may be interested in learning how you could defer capital gains, depreciation recapture, and new investment income tax on the transaction through a 1031 Exchange. If you are considering a 1031 Exchange, below are ten great questions to ask to gain a general knowledge of the 1031 Exchange process.

What is a 1031 Exchange?

A 1031 exchange, also known as a like-kind exchange, is a tax-deferred transaction that allows a real estate investor to sell qualifying property and reinvest the proceeds into other qualifying property without immediately paying capital gains taxes.

What are the main eligibility requirements for a 1031 Exchange?

To be eligible for a 1031 exchange, both the Relinquished Property (the property being sold) and the Replacement Property (the property being acquired) must be held for productive use in a trade or business or as an investment. Additionally, the properties must be of like-kind. Generally, all business or investment property is like-kind to one another, regardless of use or character. Further, the taxpayer that sells Relinquished Property must be the one taking ownership to Replacement Property; this is known as the Same Taxpayer Rule.

What types of properties qualify for a 1031 Exchange?

Any real estate property held for productive use in a trade or business or as an investment can qualify for a 1031 exchange. This includes residential rental properties, commercial properties, land, and even vacation homes if they adhere to the specific regulations on personal use time frames.

What are the time constraints for completing a 1031 Exchange?

The IRS imposes strict time constraints for completing a 1031 exchange. Once the Relinquished Property is sold, the investor has 45 calendar days to identify potential Replacement Properties and 180 calendar days to close on the purchase of one or more of those identified Replacement Properties.

What is the process for identifying Replacement Properties in a 1031 Exchange?

The investor must follow certain identification rules when identifying Replacement Property(ies). The three identification rules include: the 3-property rule (identifying up to three properties of any value); the 200% rule (identifying any number of properties as long as the total value of those properties does not exceed 200% of the value of the relinquished property); or if the taxpayer violates both of those rules, then the taxpayer needs to acquire 95% of the value of all identified properties in order to complete their 1031 exchange – 95% rule.

Can I use a Qualified Intermediary for a 1031 Exchange?

Yes, a Qualified Intermediary (QI) is typically used to facilitate a 1031 Exchange. The Qualified Intermediary (QI) is a third-party facilitator that through a series of assignments acts as the party to complete the exchange with the Exchanger. Failure to use a QI can result in missteps, causing the disqualification of the exchange and the loss of tax deferral benefits.

How does the tax deferral work in a 1031 Exchange?

In a 1031 Exchange, the capital gains taxes that would normally be owed on the sale of the Relinquished Property are deferred until the Replacement Property is sold without the use of a 1031 Exchange. If the investor continues to use 1031 Exchanges for subsequent property sales, the taxes can be deferred indefinitely.

What happens if I receive cash or other non-like-kind property in a 1031 Exchange?

If the investor receives any cash or other non-like-kind property as part of the exchange, that portion of the transaction is referred to as “boot” and would be subject to capital gains taxes.

Are there any risks associated with a 1031 Exchange?

There are risks associated with not being able to complete a valid 1031 exchange. First is the possibility that the investor may not be able to find a suitable Replacement Property within the required timeframe. Another is that the closing on the Replacement Property purchase won’t occur within the 180-day exchange period. Additionally, there remains the possibility that the investor could identify qualifying replacement property, but then not be able to negotiate the purchase of that property. It is always suggested to consult with your Legal or Tax Advisor before starting a 1031 exchange.

What are the potential benefits of a 1031 Exchange?

The potential benefits of a 1031 exchange include the ability to defer capital gains tax, depreciation recapture tax, and net investment income tax, allowing the investor to reinvest more money into a new property. Additionally, 1031 exchanges can be used to consolidate properties, diversify a real estate portfolio, relocate to a different market, or as part of an estate plan.

Does a 1031 Exchange still sound like a fit for you and your real estate transaction? Reach to our 1031 Exchange team to get the process started today! -

10 Key Questions to Ask Before Starting a 1031 Exchange

If you are looking to sell real property that was held for investment or business use, you may be interested in learning how you could defer capital gains, depreciation recapture, and new investment income tax on the transaction through a 1031 Exchange. If you are considering a 1031 Exchange, below are ten great questions to ask to gain a general knowledge of the 1031 Exchange process.

What is a 1031 Exchange?

A 1031 exchange, also known as a like-kind exchange, is a tax-deferred transaction that allows a real estate investor to sell qualifying property and reinvest the proceeds into other qualifying property without immediately paying capital gains taxes.

What are the main eligibility requirements for a 1031 Exchange?

To be eligible for a 1031 exchange, both the Relinquished Property (the property being sold) and the Replacement Property (the property being acquired) must be held for productive use in a trade or business or as an investment. Additionally, the properties must be of like-kind. Generally, all business or investment property is like-kind to one another, regardless of use or character. Further, the taxpayer that sells Relinquished Property must be the one taking ownership to Replacement Property; this is known as the Same Taxpayer Rule.

What types of properties qualify for a 1031 Exchange?

Any real estate property held for productive use in a trade or business or as an investment can qualify for a 1031 exchange. This includes residential rental properties, commercial properties, land, and even vacation homes if they adhere to the specific regulations on personal use time frames.

What are the time constraints for completing a 1031 Exchange?

The IRS imposes strict time constraints for completing a 1031 exchange. Once the Relinquished Property is sold, the investor has 45 calendar days to identify potential Replacement Properties and 180 calendar days to close on the purchase of one or more of those identified Replacement Properties.

What is the process for identifying Replacement Properties in a 1031 Exchange?

The investor must follow certain identification rules when identifying Replacement Property(ies). The three identification rules include: the 3-property rule (identifying up to three properties of any value); the 200% rule (identifying any number of properties as long as the total value of those properties does not exceed 200% of the value of the relinquished property); or if the taxpayer violates both of those rules, then the taxpayer needs to acquire 95% of the value of all identified properties in order to complete their 1031 exchange – 95% rule.

Can I use a Qualified Intermediary for a 1031 Exchange?

Yes, a Qualified Intermediary (QI) is typically used to facilitate a 1031 Exchange. The Qualified Intermediary (QI) is a third-party facilitator that through a series of assignments acts as the party to complete the exchange with the Exchanger. Failure to use a QI can result in missteps, causing the disqualification of the exchange and the loss of tax deferral benefits.

How does the tax deferral work in a 1031 Exchange?

In a 1031 Exchange, the capital gains taxes that would normally be owed on the sale of the Relinquished Property are deferred until the Replacement Property is sold without the use of a 1031 Exchange. If the investor continues to use 1031 Exchanges for subsequent property sales, the taxes can be deferred indefinitely.

What happens if I receive cash or other non-like-kind property in a 1031 Exchange?

If the investor receives any cash or other non-like-kind property as part of the exchange, that portion of the transaction is referred to as “boot” and would be subject to capital gains taxes.

Are there any risks associated with a 1031 Exchange?

There are risks associated with not being able to complete a valid 1031 exchange. First is the possibility that the investor may not be able to find a suitable Replacement Property within the required timeframe. Another is that the closing on the Replacement Property purchase won’t occur within the 180-day exchange period. Additionally, there remains the possibility that the investor could identify qualifying replacement property, but then not be able to negotiate the purchase of that property. It is always suggested to consult with your Legal or Tax Advisor before starting a 1031 exchange.

What are the potential benefits of a 1031 Exchange?

The potential benefits of a 1031 exchange include the ability to defer capital gains tax, depreciation recapture tax, and net investment income tax, allowing the investor to reinvest more money into a new property. Additionally, 1031 exchanges can be used to consolidate properties, diversify a real estate portfolio, relocate to a different market, or as part of an estate plan.

Does a 1031 Exchange still sound like a fit for you and your real estate transaction? Reach to our 1031 Exchange team to get the process started today! -

10 Key Questions to Ask Before Starting a 1031 Exchange

If you are looking to sell real property that was held for investment or business use, you may be interested in learning how you could defer capital gains, depreciation recapture, and new investment income tax on the transaction through a 1031 Exchange. If you are considering a 1031 Exchange, below are ten great questions to ask to gain a general knowledge of the 1031 Exchange process.

What is a 1031 Exchange?

A 1031 exchange, also known as a like-kind exchange, is a tax-deferred transaction that allows a real estate investor to sell qualifying property and reinvest the proceeds into other qualifying property without immediately paying capital gains taxes.

What are the main eligibility requirements for a 1031 Exchange?

To be eligible for a 1031 exchange, both the Relinquished Property (the property being sold) and the Replacement Property (the property being acquired) must be held for productive use in a trade or business or as an investment. Additionally, the properties must be of like-kind. Generally, all business or investment property is like-kind to one another, regardless of use or character. Further, the taxpayer that sells Relinquished Property must be the one taking ownership to Replacement Property; this is known as the Same Taxpayer Rule.

What types of properties qualify for a 1031 Exchange?

Any real estate property held for productive use in a trade or business or as an investment can qualify for a 1031 exchange. This includes residential rental properties, commercial properties, land, and even vacation homes if they adhere to the specific regulations on personal use time frames.

What are the time constraints for completing a 1031 Exchange?

The IRS imposes strict time constraints for completing a 1031 exchange. Once the Relinquished Property is sold, the investor has 45 calendar days to identify potential Replacement Properties and 180 calendar days to close on the purchase of one or more of those identified Replacement Properties.

What is the process for identifying Replacement Properties in a 1031 Exchange?

The investor must follow certain identification rules when identifying Replacement Property(ies). The three identification rules include: the 3-property rule (identifying up to three properties of any value); the 200% rule (identifying any number of properties as long as the total value of those properties does not exceed 200% of the value of the relinquished property); or if the taxpayer violates both of those rules, then the taxpayer needs to acquire 95% of the value of all identified properties in order to complete their 1031 exchange – 95% rule.

Can I use a Qualified Intermediary for a 1031 Exchange?

Yes, a Qualified Intermediary (QI) is typically used to facilitate a 1031 Exchange. The Qualified Intermediary (QI) is a third-party facilitator that through a series of assignments acts as the party to complete the exchange with the Exchanger. Failure to use a QI can result in missteps, causing the disqualification of the exchange and the loss of tax deferral benefits.

How does the tax deferral work in a 1031 Exchange?

In a 1031 Exchange, the capital gains taxes that would normally be owed on the sale of the Relinquished Property are deferred until the Replacement Property is sold without the use of a 1031 Exchange. If the investor continues to use 1031 Exchanges for subsequent property sales, the taxes can be deferred indefinitely.

What happens if I receive cash or other non-like-kind property in a 1031 Exchange?

If the investor receives any cash or other non-like-kind property as part of the exchange, that portion of the transaction is referred to as “boot” and would be subject to capital gains taxes.

Are there any risks associated with a 1031 Exchange?

There are risks associated with not being able to complete a valid 1031 exchange. First is the possibility that the investor may not be able to find a suitable Replacement Property within the required timeframe. Another is that the closing on the Replacement Property purchase won’t occur within the 180-day exchange period. Additionally, there remains the possibility that the investor could identify qualifying replacement property, but then not be able to negotiate the purchase of that property. It is always suggested to consult with your Legal or Tax Advisor before starting a 1031 exchange.

What are the potential benefits of a 1031 Exchange?

The potential benefits of a 1031 exchange include the ability to defer capital gains tax, depreciation recapture tax, and net investment income tax, allowing the investor to reinvest more money into a new property. Additionally, 1031 exchanges can be used to consolidate properties, diversify a real estate portfolio, relocate to a different market, or as part of an estate plan.

Does a 1031 Exchange still sound like a fit for you and your real estate transaction? Reach to our 1031 Exchange team to get the process started today! -

Transfer Taxes, “Mansion” Taxes, and 1031 Exchanges

What is a Transfer Tax?

A transfer tax is a tax imposed upon the sale or other transfer of the ownership of real property from one person or entity to another. Transfer taxes may be imposed by a state, county, or municipality, and are generally not deductible for federal income tax purposes. They can be compared to a sales tax, imposed by the government for the privilege of selling or transferring your property to someone else. In some jurisdictions, they are imposed whether you actually sell the property, or if you simply transfer it to another person or entity, such as by gift.

Not all states impose transfer taxes. Of those that do, tax rates range from 0.01% ($0.01 per $100 of transfer value) to 5% ($5.00 per $100 of transfer value). Some states impose these taxes at a flat rate, regardless of the value of the property, and a few impose a sliding scale with the tax rate increasing for higher value properties.

As mentioned above, some counties and municipalities impose their own transfer taxes, in addition to those imposed by the state. These range from 0.25% ($0.25 per $100 of transfer value) to 5% ($5.00 per $100 of transfer value).

What is a “Mansion Tax”?

The term “mansion tax” is a type of transfer tax that applies to taxes imposed on real estate transfers on high-value real estate, typically over a certain value. The tax schemes vary somewhat from state to state:Connecticut – Imposes a higher rate for properties over $800,000. For properties over $2.5 million, there is a 2.25% tax on the portion above that threshold, in addition to the regular transfer tax.

District of Columbia – Imposes a higher rate for properties over $400,000.

Hawaii – Has seven different tax rates, imposing incrementally higher rates for properties between $600,000 and $10 million.

New Jersey – Imposes a higher tax rate for homes over $350,000 plus an additional 1% to the regular transfer tax on homes over $1 million.

New York – Imposes a higher rate to homes over $1 million. New York City imposes two additional transfer taxes of up to 2.9% on homes over $2 million.

Vermont – Imposes a higher tax rate on the portion of a home’s value over $100,000.

Washington – Imposes higher tax rates for homes valued over $500,000, with increases at $1.5 million and $3 million.Recently, Los Angeles voters approved Ordinance ULA creating the so-called ULA Tax. While many people have been referring to this as a “mansion” tax, it applies to the sale or transfer of all real property over the threshold – from single-family homes to high-rise office buildings. There are a few exemptions for non-profit entities, Community Land Trusts, and Limited-Equity Housing Cooperatives. Otherwise, however, LA’s new mansion tax applies to all transfers of real property within its boundaries.

The new ULA Tax is 4% on properties valued over $5 million, and 5.5% on properties valued over $10 million. This new tax is on top of the City and County of Los Angeles transfer tax of 0.56% ($0.56 per $100 of transfer value).

How do these taxes interact with Section 1031 Exchanges?

Section 1031 exchanges are for real estate that has been held for productive use in a trade or business or for investment. Thus, they do not apply at all to a taxpayer’s primary residence, second home, or vacation home.

Further, Section 1031 only defers capital gain and depreciation recapture taxes. Transfer taxes, mansion taxes, and similar taxes imposed at the sale or transfer of property are not deferred or abated by the use of a Section 1031 exchange.

However, they are accounted for in the real estate transaction, and do reduce the amount the taxpayer must replace. Remember that for full deferral, the taxpayer should trade equal or up in fair market value. Accounting for the transfer and “mansion” taxes, we might see something like this:

Sale Price $6,000,000

Transfer Tax ( $33,000)

Mansion Tax ( $240,000)

Net $5,726,400

On this example, the taxpayer sold a $6,000,000 relinquished property, and should target a replacement property worth at least $5,726,400. This does not account for brokerage fees or other closing costs, which may also impact the taxpayer’s exchange target.

As always, taxpayers considering a Section 1031 exchange should consult with their tax and legal advisors before selling their property.