Biden’s Budget on 1031 Exchanges

The US Department of Treasury released their General Explanations of President Biden’s FY 2025 Budget, also referred to as the “Green Book”, which proposes hard limits be set on IRC Section 1031. The proposed budget suggests that 1031 Exchanges are a loophole, as they delay the payment of tax on real estate transactions as long as the Exchanger continues reinvesting in real estate. It is believed that this equates to an interest-free loan from the government, potentially indefinitely, and real estate is the only asset that gets this “sweetheart deal.” The proposal would permit deferrals of gain up to an aggregate amount of $500,000 for individuals ($1 million for married couples filing jointly) annually for similar real estate exchanges. Any gains from 1031 Exchanges above $500,000 (or $1 million for married couples filing jointly) in a year would be recognized in the year the Exchanger transfers the real property and subject to tax.

Effect on 1031 Exchanges

If a $500,000 cap on 1031 Exchanges were to be implemented, research shows it would have negative economic consequences. Below are a few of the many reasons why a $500,000 limit on 1031 Exchanges would be harmful to the economy:

Impact on Real Estate Investment and Liquidity: In real estate transactions, 1031 Exchanges are often utilized to defer capital gains taxes, motivating property owners to reinvest in other properties. However, setting a cap of $500,000 on these exchanges might hinder investors’ ability to engage in larger and more complex transactions, potentially reducing liquidity in the real estate market.

Reduced Property Transactions: A limit might dissuade property owners from engaging in 1031 Exchanges due to the potential of increased tax burdens. Consequently, this could lead to a decrease in property transactions, in turn, slowing economic activity within the real estate sector.

Potential Negative Effect on Small Businesses: Setting a limit on 1031 Exchanges could have a negative, disproportionate impact on small businesses, as well as investors who depend on 1031 Exchanges in managing their property portfolios. Biden’s cap could hinder investors’ means to expand, relocate, or optimize their property holdings.

Impact on Economic Growth: 1031 Exchange research shows that they stimulate economic growth by promoting investment, job creation, and improvements to properties, thus improvements to neighborhoods, cities, etc. Setting a hard cap on 1031 Exchanges would impede these economic accelerators.

A

Category: Company and Industry News

-

Understanding How Biden’s Proposed Budget Impacts 1031 Exchanges

-

IRS Announces Tax Relief for West Virginia Taxpayers Impacted by Severe Storms

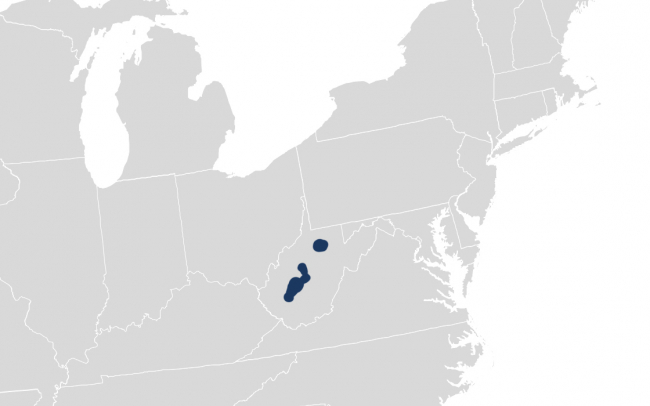

IRS has issued Tax Relief for parts of West Virginia impacted by severe storms, flooding, landslides, and mudslides that began August 28, 2023.

The General postponement date is June 17, 2024.

Individuals that reside or have businesses within Boone, Calhoun, Clay, Harrison, and Kanawha counties qualify for tax relief as this time.

An “Affected Taxpayer” includes individuals who live, and businesses whose principal place of business is located in, the Covered Disaster Area. Affected Taxpayers are entitled to relief regardless of where the relinquished property or replacement property is located. Affected Taxpayers may choose either the General Postponement relief under Section 6 OR the Alternative relief under Section 17 of Rev. Proc. 2018-58. Taxpayers who do not meet the definition of Affected Taxpayers do not qualify for Section 6 General Postponement relief.

Option One: General Postponement under Section 6 of Rev. Proc. 2018-58 (Affected Taxpayers only). Any 45-day deadline or 180-day deadline (for either a forward or reverse exchange) that falls on or after the Disaster Date above is postponed to the General Postponement Date. The General Postponement applies regardless of the date the Relinquished Property was transferred (or the parked property acquired by the EAT) and is available to Affected Taxpayers regardless of whether their exchange began before or after the Disaster Date.

Option Two: Section 17 Alternative (Available to (1) Affected Taxpayers and (2) other taxpayers who have difficulty meeting the exchange deadlines because of the disaster. See Rev. Proc. 2018-58, Section 17 for conditions constituting “difficulty”). Option Two is only available if the relinquished property was transferred (or the parked property was acquired by the EAT) on or before the Disaster Date. Any 45-day or 180-day deadline that falls on or after the Disaster Date is extended to THE LONGER OF: (1) 120 days from such deadline; OR (2) the General Postponement Date. Note the date may not be extended beyond one year or the due date (including extensions) of the tax return for the year of the disposition of the relinquished property (typically, if an extension was filed, 9/15 for corporations and partnerships and 10/15 for other taxpayers). -

IRS Announces Tax Relief for West Virginia Taxpayers Impacted by Severe Storms

IRS has issued Tax Relief for parts of West Virginia impacted by severe storms, flooding, landslides, and mudslides that began August 28, 2023.

The General postponement date is June 17, 2024.

Individuals that reside or have businesses within Boone, Calhoun, Clay, Harrison, and Kanawha counties qualify for tax relief as this time.

An “Affected Taxpayer” includes individuals who live, and businesses whose principal place of business is located in, the Covered Disaster Area. Affected Taxpayers are entitled to relief regardless of where the relinquished property or replacement property is located. Affected Taxpayers may choose either the General Postponement relief under Section 6 OR the Alternative relief under Section 17 of Rev. Proc. 2018-58. Taxpayers who do not meet the definition of Affected Taxpayers do not qualify for Section 6 General Postponement relief.

Option One: General Postponement under Section 6 of Rev. Proc. 2018-58 (Affected Taxpayers only). Any 45-day deadline or 180-day deadline (for either a forward or reverse exchange) that falls on or after the Disaster Date above is postponed to the General Postponement Date. The General Postponement applies regardless of the date the Relinquished Property was transferred (or the parked property acquired by the EAT) and is available to Affected Taxpayers regardless of whether their exchange began before or after the Disaster Date.

Option Two: Section 17 Alternative (Available to (1) Affected Taxpayers and (2) other taxpayers who have difficulty meeting the exchange deadlines because of the disaster. See Rev. Proc. 2018-58, Section 17 for conditions constituting “difficulty”). Option Two is only available if the relinquished property was transferred (or the parked property was acquired by the EAT) on or before the Disaster Date. Any 45-day or 180-day deadline that falls on or after the Disaster Date is extended to THE LONGER OF: (1) 120 days from such deadline; OR (2) the General Postponement Date. Note the date may not be extended beyond one year or the due date (including extensions) of the tax return for the year of the disposition of the relinquished property (typically, if an extension was filed, 9/15 for corporations and partnerships and 10/15 for other taxpayers). -

IRS Announces Tax Relief for West Virginia Taxpayers Impacted by Severe Storms

IRS has issued Tax Relief for parts of West Virginia impacted by severe storms, flooding, landslides, and mudslides that began August 28, 2023.

The General postponement date is June 17, 2024.

Individuals that reside or have businesses within Boone, Calhoun, Clay, Harrison, and Kanawha counties qualify for tax relief as this time.

An “Affected Taxpayer” includes individuals who live, and businesses whose principal place of business is located in, the Covered Disaster Area. Affected Taxpayers are entitled to relief regardless of where the relinquished property or replacement property is located. Affected Taxpayers may choose either the General Postponement relief under Section 6 OR the Alternative relief under Section 17 of Rev. Proc. 2018-58. Taxpayers who do not meet the definition of Affected Taxpayers do not qualify for Section 6 General Postponement relief.

Option One: General Postponement under Section 6 of Rev. Proc. 2018-58 (Affected Taxpayers only). Any 45-day deadline or 180-day deadline (for either a forward or reverse exchange) that falls on or after the Disaster Date above is postponed to the General Postponement Date. The General Postponement applies regardless of the date the Relinquished Property was transferred (or the parked property acquired by the EAT) and is available to Affected Taxpayers regardless of whether their exchange began before or after the Disaster Date.

Option Two: Section 17 Alternative (Available to (1) Affected Taxpayers and (2) other taxpayers who have difficulty meeting the exchange deadlines because of the disaster. See Rev. Proc. 2018-58, Section 17 for conditions constituting “difficulty”). Option Two is only available if the relinquished property was transferred (or the parked property was acquired by the EAT) on or before the Disaster Date. Any 45-day or 180-day deadline that falls on or after the Disaster Date is extended to THE LONGER OF: (1) 120 days from such deadline; OR (2) the General Postponement Date. Note the date may not be extended beyond one year or the due date (including extensions) of the tax return for the year of the disposition of the relinquished property (typically, if an extension was filed, 9/15 for corporations and partnerships and 10/15 for other taxpayers). -

A Year In Review: 2023

2023 was a year of unknowns for much of the real estate industry and adjacent industries like 1031 Exchange Qualified Intermediaries. With interest rates reaching a 20 year high, recession, inflation, all while real estate prices held steady and high – it was a challenging market for many.

Accruit’s team didn’t let these factors impact their goals for growth and innovation. It was a great 2023 and Accruit’s team couldn’t be more proud of the results.

The material in this blog is presented for informational purposes only. The information presented is not investment, legal, tax or compliance advice. Accruit performs the duties of a Qualified Intermediary, and as such does not offer or sell investments or provide investment, legal, or tax advice.

-

A Year In Review: 2023

2023 was a year of unknowns for much of the real estate industry and adjacent industries like 1031 Exchange Qualified Intermediaries. With interest rates reaching a 20 year high, recession, inflation, all while real estate prices held steady and high – it was a challenging market for many.

Accruit’s team didn’t let these factors impact their goals for growth and innovation. It was a great 2023 and Accruit’s team couldn’t be more proud of the results.

The material in this blog is presented for informational purposes only. The information presented is not investment, legal, tax or compliance advice. Accruit performs the duties of a Qualified Intermediary, and as such does not offer or sell investments or provide investment, legal, or tax advice.

-

A Year In Review: 2023

2023 was a year of unknowns for much of the real estate industry and adjacent industries like 1031 Exchange Qualified Intermediaries. With interest rates reaching a 20 year high, recession, inflation, all while real estate prices held steady and high – it was a challenging market for many.

Accruit’s team didn’t let these factors impact their goals for growth and innovation. It was a great 2023 and Accruit’s team couldn’t be more proud of the results.

The material in this blog is presented for informational purposes only. The information presented is not investment, legal, tax or compliance advice. Accruit performs the duties of a Qualified Intermediary, and as such does not offer or sell investments or provide investment, legal, or tax advice.

-

IRS Announces Tax Relief for Multiple Tennessee Counties Impacted by Recent Tornados

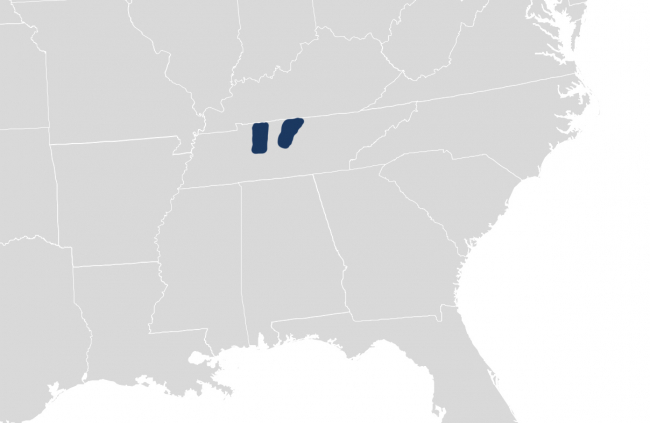

Due to recent storms and tornados, the IRS has issued Tax Relief for parts of Tennessee.

The General postponement date is June 17, 2024.

Individuals that reside or have businesses within Davidson, Dickson, Montgomery, and Sumner counties qualify for tax relief as this time.

An “Affected Taxpayer” includes individuals who live, and businesses whose principal place of business is located in, the Covered Disaster Area. Affected Taxpayers are entitled to relief regardless of where the relinquished property or replacement property is located. Affected Taxpayers may choose either the General Postponement relief under Section 6 OR the Alternative relief under Section 17 of Rev. Proc. 2018-58. Taxpayers who do not meet the definition of Affected Taxpayers do not qualify for Section 6 General Postponement relief.

Option One: General Postponement under Section 6 of Rev. Proc. 2018-58 (Affected Taxpayers only). Any 45-day deadline or 180-day deadline (for either a forward or reverse exchange) that falls on or after the Disaster Date above is postponed to the General Postponement Date. The General Postponement applies regardless of the date the Relinquished Property was transferred (or the parked property acquired by the EAT) and is available to Affected Taxpayers regardless of whether their exchange began before or after the Disaster Date.

Option Two: Section 17 Alternative (Available to (1) Affected Taxpayers and (2) other taxpayers who have difficulty meeting the exchange deadlines because of the disaster. See Rev. Proc. 2018-58, Section 17 for conditions constituting “difficulty”). Option Two is only available if the relinquished property was transferred (or the parked property was acquired by the EAT) on or before the Disaster Date. Any 45-day or 180-day deadline that falls on or after the Disaster Date is extended to THE LONGER OF: (1) 120 days from such deadline; OR (2) the General Postponement Date. Note the date may not be extended beyond one year or the due date (including extensions) of the tax return for the year of the disposition of the relinquished property (typically, if an extension was filed, 9/15 for corporations and partnerships and 10/15 for other taxpayers). -

IRS Announces Tax Relief for Multiple Tennessee Counties Impacted by Recent Tornados

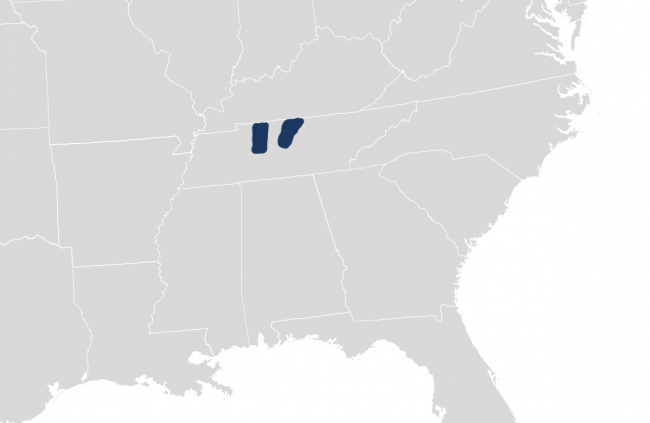

Due to recent storms and tornados, the IRS has issued Tax Relief for parts of Tennessee.

The General postponement date is June 17, 2024.

Individuals that reside or have businesses within Davidson, Dickson, Montgomery, and Sumner counties qualify for tax relief as this time.

An “Affected Taxpayer” includes individuals who live, and businesses whose principal place of business is located in, the Covered Disaster Area. Affected Taxpayers are entitled to relief regardless of where the relinquished property or replacement property is located. Affected Taxpayers may choose either the General Postponement relief under Section 6 OR the Alternative relief under Section 17 of Rev. Proc. 2018-58. Taxpayers who do not meet the definition of Affected Taxpayers do not qualify for Section 6 General Postponement relief.

Option One: General Postponement under Section 6 of Rev. Proc. 2018-58 (Affected Taxpayers only). Any 45-day deadline or 180-day deadline (for either a forward or reverse exchange) that falls on or after the Disaster Date above is postponed to the General Postponement Date. The General Postponement applies regardless of the date the Relinquished Property was transferred (or the parked property acquired by the EAT) and is available to Affected Taxpayers regardless of whether their exchange began before or after the Disaster Date.

Option Two: Section 17 Alternative (Available to (1) Affected Taxpayers and (2) other taxpayers who have difficulty meeting the exchange deadlines because of the disaster. See Rev. Proc. 2018-58, Section 17 for conditions constituting “difficulty”). Option Two is only available if the relinquished property was transferred (or the parked property was acquired by the EAT) on or before the Disaster Date. Any 45-day or 180-day deadline that falls on or after the Disaster Date is extended to THE LONGER OF: (1) 120 days from such deadline; OR (2) the General Postponement Date. Note the date may not be extended beyond one year or the due date (including extensions) of the tax return for the year of the disposition of the relinquished property (typically, if an extension was filed, 9/15 for corporations and partnerships and 10/15 for other taxpayers). -

IRS Announces Tax Relief for Multiple Tennessee Counties Impacted by Recent Tornados

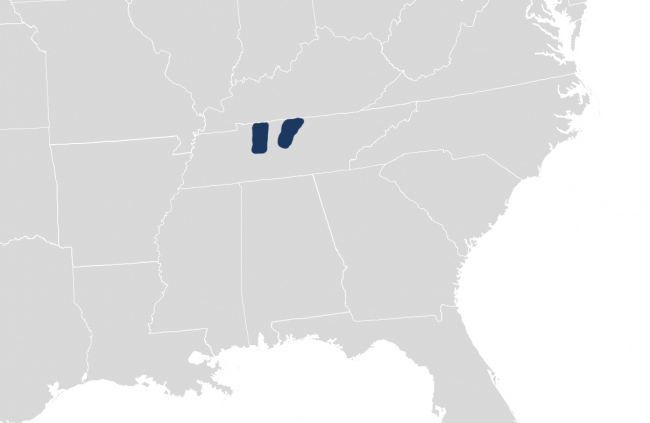

Due to recent storms and tornados, the IRS has issued Tax Relief for parts of Tennessee.

The General postponement date is June 17, 2024.

Individuals that reside or have businesses within Davidson, Dickson, Montgomery, and Sumner counties qualify for tax relief as this time.

An “Affected Taxpayer” includes individuals who live, and businesses whose principal place of business is located in, the Covered Disaster Area. Affected Taxpayers are entitled to relief regardless of where the relinquished property or replacement property is located. Affected Taxpayers may choose either the General Postponement relief under Section 6 OR the Alternative relief under Section 17 of Rev. Proc. 2018-58. Taxpayers who do not meet the definition of Affected Taxpayers do not qualify for Section 6 General Postponement relief.

Option One: General Postponement under Section 6 of Rev. Proc. 2018-58 (Affected Taxpayers only). Any 45-day deadline or 180-day deadline (for either a forward or reverse exchange) that falls on or after the Disaster Date above is postponed to the General Postponement Date. The General Postponement applies regardless of the date the Relinquished Property was transferred (or the parked property acquired by the EAT) and is available to Affected Taxpayers regardless of whether their exchange began before or after the Disaster Date.

Option Two: Section 17 Alternative (Available to (1) Affected Taxpayers and (2) other taxpayers who have difficulty meeting the exchange deadlines because of the disaster. See Rev. Proc. 2018-58, Section 17 for conditions constituting “difficulty”). Option Two is only available if the relinquished property was transferred (or the parked property was acquired by the EAT) on or before the Disaster Date. Any 45-day or 180-day deadline that falls on or after the Disaster Date is extended to THE LONGER OF: (1) 120 days from such deadline; OR (2) the General Postponement Date. Note the date may not be extended beyond one year or the due date (including extensions) of the tax return for the year of the disposition of the relinquished property (typically, if an extension was filed, 9/15 for corporations and partnerships and 10/15 for other taxpayers).