Due to seawater intrusion, the IRS has issued Tax Relief for parts of Louisiana.

The General postponement date is February 15, 2024.

Individuals that reside or have a business within Jefferson, Orleans, Plaquemines, and St. Bernard parishes in Louisiana qualify for tax relief.

An “Affected Taxpayer” includes individuals who live, and businesses whose principal place of business is located in, the Covered Disaster Area. Affected Taxpayers are entitled to relief regardless of where the relinquished property or replacement property is located. Affected Taxpayers may choose either the General Postponement relief under Section 6 OR the Alternative relief under Section 17 of Rev. Proc. 2018-58. Taxpayers who do not meet the definition of Affected Taxpayers do not qualify for Section 6 General Postponement relief.

Option One: General Postponement under Section 6 of Rev. Proc. 2018-58 (Affected Taxpayers only). Any 45-day deadline or 180-day deadline (for either a forward or reverse exchange) that falls on or after the Disaster Date above is postponed to the General Postponement Date. The General Postponement applies regardless of the date the Relinquished Property was transferred (or the parked property acquired by the EAT) and is available to Affected Taxpayers regardless of whether their exchange began before or after the Disaster Date.

Option Two: Section 17 Alternative (Available to (1) Affected Taxpayers and (2) other taxpayers who have difficulty meeting the exchange deadlines because of the disaster. See Rev. Proc. 2018-58, Section 17 for conditions constituting “difficulty”). Option Two is only available if the relinquished property was transferred (or the parked property was acquired by the EAT) on or before the Disaster Date. Any 45-day or 180-day deadline that falls on or after the Disaster Date is extended to THE LONGER OF: (1) 120 days from such deadline; OR (2) the General Postponement Date. Note the date may not be extended beyond one year or the due date (including extensions) of the tax return for the year of the disposition of the relinquished property (typically, if an extension was filed, 9/15 for corporations and partnerships and 10/15 for other taxpayers).

Blog

-

IRS Announces Tax Relief for Parts of Louisiana by to seawater intrusion

-

IRS Announces Tax Relief for Parts of Louisiana by to seawater intrusion

Due to seawater intrusion, the IRS has issued Tax Relief for parts of Louisiana.

The General postponement date is February 15, 2024.

Individuals that reside or have a business within Jefferson, Orleans, Plaquemines, and St. Bernard parishes in Louisiana qualify for tax relief.

An “Affected Taxpayer” includes individuals who live, and businesses whose principal place of business is located in, the Covered Disaster Area. Affected Taxpayers are entitled to relief regardless of where the relinquished property or replacement property is located. Affected Taxpayers may choose either the General Postponement relief under Section 6 OR the Alternative relief under Section 17 of Rev. Proc. 2018-58. Taxpayers who do not meet the definition of Affected Taxpayers do not qualify for Section 6 General Postponement relief.

Option One: General Postponement under Section 6 of Rev. Proc. 2018-58 (Affected Taxpayers only). Any 45-day deadline or 180-day deadline (for either a forward or reverse exchange) that falls on or after the Disaster Date above is postponed to the General Postponement Date. The General Postponement applies regardless of the date the Relinquished Property was transferred (or the parked property acquired by the EAT) and is available to Affected Taxpayers regardless of whether their exchange began before or after the Disaster Date.

Option Two: Section 17 Alternative (Available to (1) Affected Taxpayers and (2) other taxpayers who have difficulty meeting the exchange deadlines because of the disaster. See Rev. Proc. 2018-58, Section 17 for conditions constituting “difficulty”). Option Two is only available if the relinquished property was transferred (or the parked property was acquired by the EAT) on or before the Disaster Date. Any 45-day or 180-day deadline that falls on or after the Disaster Date is extended to THE LONGER OF: (1) 120 days from such deadline; OR (2) the General Postponement Date. Note the date may not be extended beyond one year or the due date (including extensions) of the tax return for the year of the disposition of the relinquished property (typically, if an extension was filed, 9/15 for corporations and partnerships and 10/15 for other taxpayers). -

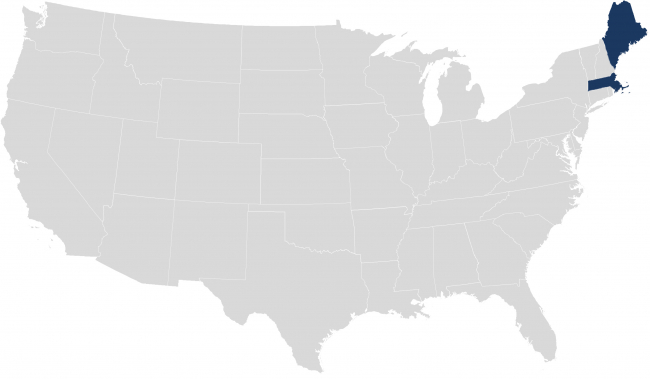

IRS Announces Tax Relief for Maine and Massachusetts Due to Hurricane Lee

Due to Hurricane Lee, the IRS has issued Tax Relief for Maine and Massachusetts.

The General postponement date is February 15, 2024.

All 16 counties in Maine and all 14 counties in Massachusetts qualify for tax relief.

An “Affected Taxpayer” includes individuals who live, and businesses whose principal place of business is located in, the Covered Disaster Area. Affected Taxpayers are entitled to relief regardless of where the relinquished property or replacement property is located. Affected Taxpayers may choose either the General Postponement relief under Section 6 OR the Alternative relief under Section 17 of Rev. Proc. 2018-58. Taxpayers who do not meet the definition of Affected Taxpayers do not qualify for Section 6 General Postponement relief.

Option One: General Postponement under Section 6 of Rev. Proc. 2018-58 (Affected Taxpayers only). Any 45-day deadline or 180-day deadline (for either a forward or reverse exchange) that falls on or after the Disaster Date above is postponed to the General Postponement Date. The General Postponement applies regardless of the date the Relinquished Property was transferred (or the parked property acquired by the EAT) and is available to Affected Taxpayers regardless of whether their exchange began before or after the Disaster Date.

Option Two: Section 17 Alternative (Available to (1) Affected Taxpayers and (2) other taxpayers who have difficulty meeting the exchange deadlines because of the disaster. See Rev. Proc. 2018-58, Section 17 for conditions constituting “difficulty”). Option Two is only available if the relinquished property was transferred (or the parked property was acquired by the EAT) on or before the Disaster Date. Any 45-day or 180-day deadline that falls on or after the Disaster Date is extended to THE LONGER OF: (1) 120 days from such deadline; OR (2) the General Postponement Date. Note the date may not be extended beyond one year or the due date (including extensions) of the tax return for the year of the disposition of the relinquished property (typically, if an extension was filed, 9/15 for corporations and partnerships and 10/15 for other taxpayers). -

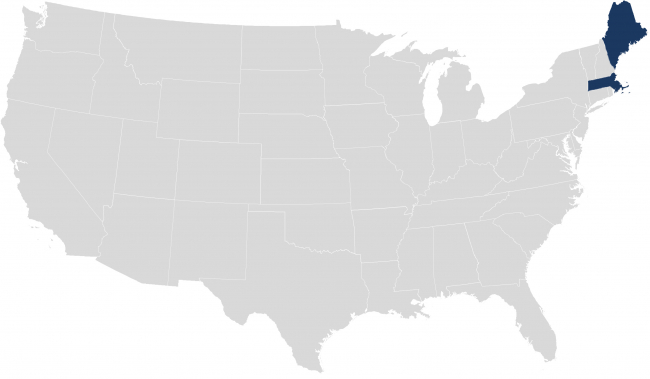

IRS Announces Tax Relief for Maine and Massachusetts Due to Hurricane Lee

Due to Hurricane Lee, the IRS has issued Tax Relief for Maine and Massachusetts.

The General postponement date is February 15, 2024.

All 16 counties in Maine and all 14 counties in Massachusetts qualify for tax relief.

An “Affected Taxpayer” includes individuals who live, and businesses whose principal place of business is located in, the Covered Disaster Area. Affected Taxpayers are entitled to relief regardless of where the relinquished property or replacement property is located. Affected Taxpayers may choose either the General Postponement relief under Section 6 OR the Alternative relief under Section 17 of Rev. Proc. 2018-58. Taxpayers who do not meet the definition of Affected Taxpayers do not qualify for Section 6 General Postponement relief.

Option One: General Postponement under Section 6 of Rev. Proc. 2018-58 (Affected Taxpayers only). Any 45-day deadline or 180-day deadline (for either a forward or reverse exchange) that falls on or after the Disaster Date above is postponed to the General Postponement Date. The General Postponement applies regardless of the date the Relinquished Property was transferred (or the parked property acquired by the EAT) and is available to Affected Taxpayers regardless of whether their exchange began before or after the Disaster Date.

Option Two: Section 17 Alternative (Available to (1) Affected Taxpayers and (2) other taxpayers who have difficulty meeting the exchange deadlines because of the disaster. See Rev. Proc. 2018-58, Section 17 for conditions constituting “difficulty”). Option Two is only available if the relinquished property was transferred (or the parked property was acquired by the EAT) on or before the Disaster Date. Any 45-day or 180-day deadline that falls on or after the Disaster Date is extended to THE LONGER OF: (1) 120 days from such deadline; OR (2) the General Postponement Date. Note the date may not be extended beyond one year or the due date (including extensions) of the tax return for the year of the disposition of the relinquished property (typically, if an extension was filed, 9/15 for corporations and partnerships and 10/15 for other taxpayers). -

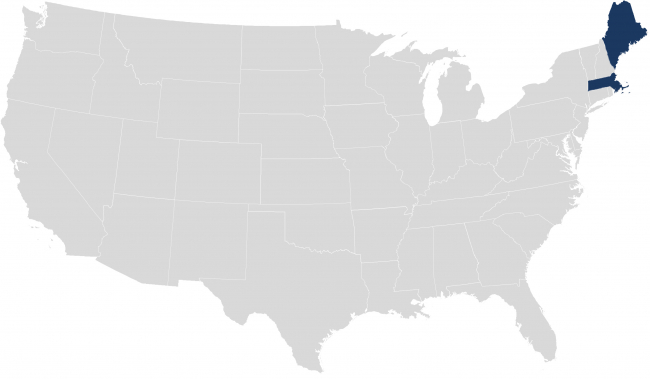

IRS Announces Tax Relief for Maine and Massachusetts Due to Hurricane Lee

Due to Hurricane Lee, the IRS has issued Tax Relief for Maine and Massachusetts.

The General postponement date is February 15, 2024.

All 16 counties in Maine and all 14 counties in Massachusetts qualify for tax relief.

An “Affected Taxpayer” includes individuals who live, and businesses whose principal place of business is located in, the Covered Disaster Area. Affected Taxpayers are entitled to relief regardless of where the relinquished property or replacement property is located. Affected Taxpayers may choose either the General Postponement relief under Section 6 OR the Alternative relief under Section 17 of Rev. Proc. 2018-58. Taxpayers who do not meet the definition of Affected Taxpayers do not qualify for Section 6 General Postponement relief.

Option One: General Postponement under Section 6 of Rev. Proc. 2018-58 (Affected Taxpayers only). Any 45-day deadline or 180-day deadline (for either a forward or reverse exchange) that falls on or after the Disaster Date above is postponed to the General Postponement Date. The General Postponement applies regardless of the date the Relinquished Property was transferred (or the parked property acquired by the EAT) and is available to Affected Taxpayers regardless of whether their exchange began before or after the Disaster Date.

Option Two: Section 17 Alternative (Available to (1) Affected Taxpayers and (2) other taxpayers who have difficulty meeting the exchange deadlines because of the disaster. See Rev. Proc. 2018-58, Section 17 for conditions constituting “difficulty”). Option Two is only available if the relinquished property was transferred (or the parked property was acquired by the EAT) on or before the Disaster Date. Any 45-day or 180-day deadline that falls on or after the Disaster Date is extended to THE LONGER OF: (1) 120 days from such deadline; OR (2) the General Postponement Date. Note the date may not be extended beyond one year or the due date (including extensions) of the tax return for the year of the disposition of the relinquished property (typically, if an extension was filed, 9/15 for corporations and partnerships and 10/15 for other taxpayers). -

How to Utilize a 1031 Exchange on Related Party or Same Taxpayer Property

With interest rates at a 15-year high and real estate values resisting a turn to the downside, purchasing Replacement Property, especially one that requires financing, isn’t as attractive as it was previously in lower interest rate market environments.

An alternative option for Taxpayers is exploring the possibility of a Leasehold Improvement Exchange, accommodated by an Accruit-owned entity, on a newly created long-term leasehold interest.

In 2000, the IRS issued Revenue Procedure 2000-37, which created a “safe harbor” for certain “parking” arrangements (i.e., where an accommodator temporarily holds title to exchange property), including Improvement Exchanges where a taxpayer desires to spend exchange value making improvements to Replacement Property.

A Leasehold Improvement Exchange is a variation of the kind of parking arrangement (i.e. reverse exchange) most used when a Related Party owns the base Replacement Property. Since, subject to limited exceptions outside the purview of this article, a Taxpayer cannot acquire a fee simple interest in real property from a Related Party.

In addition, although not a Leasehold Improvement issue, a Taxpayer cannot improve property once acquired by the Taxpayer, even if acquired from an unrelated party. The use of a parking arrangement is required if the Taxpayer plans to use exchange value to improve a real property interest.

This article outlines the planning, structuring, and regulation implicated when contemplating a Leasehold Improvement Exchange.

What is a Related Party to the Taxpayer?

The first step in structuring a Leasehold Improvement Exchange is understanding how the regulations define a Related Party. For purposes of § 1031(f), the term “related person” means any person bearing a relationship to the Taxpayer described in § 267(b) or 707(b)(1). The most common Related Parties implicated in a Leasehold Improvement Exchange are as follows:Members of the same family unit (siblings, spouse, ancestors, and lineal descendants);

Two partnerships in which the same person or persons own, directly or indirectly, more than a 50% capital interest or a 50% profits interest, in both partnerships;

A partnership and a person owning, directly or indirectly, more than a 50% capital interest or a 50% profits interest, in such partnership;

A corporation and a partnership if the same person or persons own: more than 50% in value of the outstanding stock of the corporation, and more than 50% of the capital interest, or the profits interest, in the partnership; and

Two corporations that are in the same controlled group.Read our extensive Related Party article for a more in-depth explanation of Related Party in relation to a 1031 Exchange.

Process of Leasehold Improvement Exchange

The structure of a Leasehold Improvement Exchange involves an Accommodator (as opposed to a Qualified Intermediary, which serves a different exchange function) carving out and acquiring a long-term interest in a ground lease from the fee simple owner of the land (i.e. the Related Party). The Accommodator would be a newly created Accruit-owned special purpose limited liability company specific for the transaction. The Accommodator uses the exchange value to pay construction and material invoices and incorporate specified tenant improvements on the ground lease. The source of Accommodator financing to pay for these costs may originate from exchange funds, bridge financing, and/or cash from the taxpayer.

The lease from the Related Party as lessor to the Accommodator as lessee must be a fair market lease supported by fair market rent to be paid by the lessee to the ground lessor. Under the safe harbor of the Reverse Exchange regulations promulgated in Rev. Proc. 2000-37, the rent expense can be lent from the Taxpayer to the Accommodator.

At the conclusion, after the necessary exchange value is injected into tenant improvements or prior to the 180th day, whichever occurs first, the Taxpayer acquires the interest in the long-term lease and newly constructed improvements from the Accommodator using funds generated from the sale of the Relinquished Property. Any applicable bridge loans are paid down or satisfied using these funds. As a result, the Replacement Property is the: (1) improvements acquired from the Accommodator; and (2) the long-term leasehold interest. Of note, the Taxpayer will only be able to acquire and receive credit for the tenant improvements, materials, and workmanship which are vertical and incorporated into the leasehold estate prior to the 180th day, but will not be able to allocate exchange value to those materials still on the worksite nor pre-pay the contractor.

Upon conveyance from the Accommodator to the Taxpayer, the leasehold interest and term must:Have 30 years or more remaining on the term upon transfer to the Taxpayer as Replacement Property (or 39 years if the replacement property improvements are commercial in nature); and

Remain in place for a period of time, usually two years or more, after the exchange concludes with rent flowing from tenant to landlord.Exchange commentators agree that these kinds of Related Party Leasehold Improvement Exchanges can be structured within the safe harbor, provided the Taxpayer acquires the leasehold interest plus improvements within 180 days of commencing the exchange. Several IRS private letter rulings also approve this structure including: LTR 201408019 (Feb. 21, 2014); LTR 200251008 (Dec. 20, 2002); and LTR 200329021 (Jul. 18, 2003).

Gain a better understanding of the process through this flyer, Leasehold Improvement Exchange.

What if the Same Taxpayer owns both the Relinquished and Replacement Properties?

As you likely surmised, the first step in this type of 1031 exchange is identifying the tax owner of the Relinquished Property and the Replacement Property.

If those two entities or individuals are the same Taxpayer, then it’s necessary to take sufficient advance planning steps to inject a Related Party into the proposed transaction. To successfully structure a Leasehold Improvement Exchange, there are several methods for incorporating a Related Party into the proposed transaction. I will outline one such technique below. However, before doing so, we must discuss some issues implicated under the 1031 Exchange regulations when proceeding with a Leasehold Improvement Exchange.

When the Same Taxpayer owns not only the land on which improvements are to be built, but also the Relinquished Property(ies), issues present such as the “exchange” requirement, which requires a reciprocal transfer of property between two separate parties. Also raised in these scenarios is the “like-kind” requirement. Navigating each of these elements is vital for a successful exchange and requires advance planning and an independent business purpose.

“Like-Kind” Requirement

As for the “like-kind” requirement, while the acquisition of the newly constructed improvements are acquired from the Accommodator (rather than the Taxpayer) and may otherwise satisfy the exchange requirement, the IRS takes the position that improvements to existing real property alone, absent the acquisition of an interest in the underlying land, is not “like-kind” to a fee simple interest in real property. For example, to satisfy the “like-kind” standard, the improvements must be tethered to a real property interest. To that point, the IRS has taken the position that the assignment of a lessee’s interest in a lease of greater than 30 years, including options, to an exchanging Taxpayer is “like-kind” to a fee simple interest. Rev. Rul. 68-394. W

An additional issue surfaces when the Same Taxpayer owns the Replacement Property within 180 days of the Accommodator carving out a newly created leasehold interest to begin the parking arrangement. In Rev. Proc. 2004-51, the IRS specifically modified Rev. Proc. 2000-37 and excluded from the safe harbor parking arrangements where the Same Taxpayer owns Replacement Property during the 180-day period ending on the date the Accommodator acquires an “interest” in that property. Under this rule, an “interest” in the property is arguably a newly created leasehold estate because that interest is conveyed to the Accommodator from the fee simple owner of the base property. This 180-day look-back period means that simply transferring land to a Related Party and immediately commencing a parking arrangement may not be a viable strategy.

Within Rev. Proc. 2004-51 the IRS and Treasury indicated they are:

“…continuing to study parking transactions, including transactions in which a person related to the taxpayer transfers a leasehold in land to an accommodation party and the accommodation party makes improvements to the land and transfers the leasehold with the improvements to the taxpayer in exchange for other real estate. Rev. Proc. 2004-51, 2004-2 CB 294 §2.06.”

So, although there may be an elevated risk of adverse exchange treatment where the Same Taxpayer owns Replacement Property per the rules and requirements outlined above, some possible resolutions exist. One such resolution is to have the Taxpayer contribute the Replacement base Property to a Related Party or different Taxpayer greater than 180 days prior to commencing the parking arrangement. After the lapse of 181 days, the Accommodator would then carve out a long-term leasehold (30 year or greater) directly with the Related Party and build out tenant improvements. Since the modification under Rev. Proc 2004-51 limits the look-back period to a definite time period (rather than disqualifying all property ever owned by a Taxpayer), it appears that if structured this way a subsequent Leasehold Improvement Exchange could be completed within the safe harbor.

“Independent Business Purpose” Requirement

An additional consideration when transferring the fee simple interest to a Related Party in advance of a Leasehold Improvement Exchange, is the independent business purpose requirement. Under this requirement, any transfer should be supported by an independent non-tax related business purpose. If no such independent business purpose exists for the transfer, then the theoretical risk is that the IRS would disregard the transfer and would still consider the Taxpayer to be the tax owner fee simple interest.

Some exchange commentators take the position an independent business purpose could perhaps be evidenced by: (1) additional liability protection as to a Taxpayer’s other assets; or (2) a need to establish a separate entity for holding only the fee simple interest in land as opposed to developing and leasing new improvements initiating a need for new management responsibilities. We defer to the Taxpayer’s advisors to determine whether there exists an independent business purpose for the change of ownership.

As discussed, this resolution is designed to preserve the “exchange” requirement, the “like-kind” requirement, the 180-day look-back under Rev. Proc. 2004-51, and to prevent “merger of title.” Merger of title is yet another factor in the analysis and occurs when the Accommodator steps out following construction and conveys a long-term leasehold interest and tenant improvements to the Taxpayer who finds themselves as both tenant (lessee) and landlord (lessor) under the lease agreement. In this scenario, by Operation of Law, merger of the leasehold interest with the fee simple interest occurs, thereby destroying the leasehold interest tethered to the improvements which is vital to preserve the like-kind requirement referenced above.

However, when a Related Party is involved as the landlord, then the title to the fee simple interest and long-term leasehold interest will not merge because there are separate and distinct tax owners on either side of the lease. In other words, the Taxpayer did not receive a non-permitted interest from a related party, rather he received the leasehold improvements solely from the EAT.

Example of a Leasehold Used in a 1031 Exchange

Mr. Rancher owns several properties in Southeast Colorado under his single-member LLC: SE Cattle Company, LLC. One such property is a debt free 80-acre tract of land with a calving barn for 200 head of cattle. Mr. Rancher is offered above market value for his 80-acre tract from a large retail distribution center. His temptation to capitalize on the offer is restrained by concern for high interest rates on new debt, low inventory, and above market asking prices on possible Replacement Property. As a result, he may not be able find a suitable Replacement Property should he accept the offer from the prospective buyer.

Nevertheless, Mr. Rancher’s daughter, a Related Party, owns a separate and distinct 150-acres of land in Colorado which needs substantial improvements for a newly anticipated horse arena, state-of-the-art calving barn, and fencing for up to 300 head of cattle.

Mr. Rancher’s local CPA recommends he contact a 1031 Exchange Qualified Intermediary well versed in ag-related property transactions to see if they have any ideas or solutions for his current dilemma.

Upon discussing his situation with one of Accruit’s staff attorneys, Mr. Rancher learns he can engage the services of Accruit as a Qualified Intermediary (“QI”) and as an Exchange Accommodation Titleholder (“EAT”), the latter of which is wholly owned by Accruit Exchange Accommodation Services, LLC, to facilitate a Leasehold Improvement Exchange. Mr. Rancher decides to initiate the proposed 1031 Exchange and accepts the $897,000.00 offer on his 80-acre tract. After closing costs, $871,000.00 in net exchange proceeds are held with the QI for the benefit of SE Cattle Company, LLC. Immediately thereafter, the EAT carves out and acquires a newly created long-term leasehold interest from Mr. Rancher’s daughter who serves as the lessor (i.e. landlord).

Through a Leasehold Improvement Exchange, SE Cattle Company, LLC, will authorize the QI to make progress payments to the EAT for constructing tenant improvements including a horse arena, state-of-the-art calving barn, and fencing for up to 300 head of cattle. The EAT then spends the $871,000.00 for construction costs within 180 days following the closing date of the 80-acre tract. Upon completion, the long-term leasehold interest and newly constructed tenant improvements are assigned by the EAT to SE Cattle Company, LLC, as like-kind Replacement Property prior to the 180th day following the closing on the Relinquished Property.

Mr. Rancher was able to utilize a long-term leasehold on property owned by a Related Party to complete a Leasehold Improvement Exchange and capitalize on all the benefits a 1031 Exchange has to offer, most notably deferring various level of tax including depreciation recapture, capital gains, applicable state taxes, and net investment income tax.

Summary

In conclusion, a Leasehold Improvement Exchange provides an opportunity to take advantage of the tax deferral benefits a 1031 Exchange offers when an investor holds multiple properties. An important takeaway is that proper planning and adequate lead time are required to ensure an exchange involving a long-term leasehold is structured properly.

The key is advance planning, and it is vital to have the experience of an Accruit subject-matter expert to structure a Leasehold Improvement Exchange. While it may seem overwhelming, these exchanges are common, and they provide the Taxpayer with great optionality, and can be completed within the safe harbor of Rev. Proc. 2000-37. Accruit staff attorneys have many other structuring possibilities that we can provide additional insight on for your consideration.

As always, we encourage property owners to invoke the advice of their attorneys, financial advisors, and CPA when considering any disposition of property.

The material in this blog is presented for informational purposes only. The information presented is not investment, legal, tax or compliance advice. Accruit performs the duties of a Qualified Intermediary, and as such does not offer or sell investments or provide investment, legal, or tax advice. -

How to Utilize a 1031 Exchange on Related Party or Same Taxpayer Property

With interest rates at a 15-year high and real estate values resisting a turn to the downside, purchasing Replacement Property, especially one that requires financing, isn’t as attractive as it was previously in lower interest rate market environments.

An alternative option for Taxpayers is exploring the possibility of a Leasehold Improvement Exchange, accommodated by an Accruit-owned entity, on a newly created long-term leasehold interest.

In 2000, the IRS issued Revenue Procedure 2000-37, which created a “safe harbor” for certain “parking” arrangements (i.e., where an accommodator temporarily holds title to exchange property), including Improvement Exchanges where a taxpayer desires to spend exchange value making improvements to Replacement Property.

A Leasehold Improvement Exchange is a variation of the kind of parking arrangement (i.e. reverse exchange) most used when a Related Party owns the base Replacement Property. Since, subject to limited exceptions outside the purview of this article, a Taxpayer cannot acquire a fee simple interest in real property from a Related Party.

In addition, although not a Leasehold Improvement issue, a Taxpayer cannot improve property once acquired by the Taxpayer, even if acquired from an unrelated party. The use of a parking arrangement is required if the Taxpayer plans to use exchange value to improve a real property interest.

This article outlines the planning, structuring, and regulation implicated when contemplating a Leasehold Improvement Exchange.

What is a Related Party to the Taxpayer?

The first step in structuring a Leasehold Improvement Exchange is understanding how the regulations define a Related Party. For purposes of § 1031(f), the term “related person” means any person bearing a relationship to the Taxpayer described in § 267(b) or 707(b)(1). The most common Related Parties implicated in a Leasehold Improvement Exchange are as follows:Members of the same family unit (siblings, spouse, ancestors, and lineal descendants);

Two partnerships in which the same person or persons own, directly or indirectly, more than a 50% capital interest or a 50% profits interest, in both partnerships;

A partnership and a person owning, directly or indirectly, more than a 50% capital interest or a 50% profits interest, in such partnership;

A corporation and a partnership if the same person or persons own: more than 50% in value of the outstanding stock of the corporation, and more than 50% of the capital interest, or the profits interest, in the partnership; and

Two corporations that are in the same controlled group.Read our extensive Related Party article for a more in-depth explanation of Related Party in relation to a 1031 Exchange.

Process of Leasehold Improvement Exchange

The structure of a Leasehold Improvement Exchange involves an Accommodator (as opposed to a Qualified Intermediary, which serves a different exchange function) carving out and acquiring a long-term interest in a ground lease from the fee simple owner of the land (i.e. the Related Party). The Accommodator would be a newly created Accruit-owned special purpose limited liability company specific for the transaction. The Accommodator uses the exchange value to pay construction and material invoices and incorporate specified tenant improvements on the ground lease. The source of Accommodator financing to pay for these costs may originate from exchange funds, bridge financing, and/or cash from the taxpayer.

The lease from the Related Party as lessor to the Accommodator as lessee must be a fair market lease supported by fair market rent to be paid by the lessee to the ground lessor. Under the safe harbor of the Reverse Exchange regulations promulgated in Rev. Proc. 2000-37, the rent expense can be lent from the Taxpayer to the Accommodator.

At the conclusion, after the necessary exchange value is injected into tenant improvements or prior to the 180th day, whichever occurs first, the Taxpayer acquires the interest in the long-term lease and newly constructed improvements from the Accommodator using funds generated from the sale of the Relinquished Property. Any applicable bridge loans are paid down or satisfied using these funds. As a result, the Replacement Property is the: (1) improvements acquired from the Accommodator; and (2) the long-term leasehold interest. Of note, the Taxpayer will only be able to acquire and receive credit for the tenant improvements, materials, and workmanship which are vertical and incorporated into the leasehold estate prior to the 180th day, but will not be able to allocate exchange value to those materials still on the worksite nor pre-pay the contractor.

Upon conveyance from the Accommodator to the Taxpayer, the leasehold interest and term must:Have 30 years or more remaining on the term upon transfer to the Taxpayer as Replacement Property (or 39 years if the replacement property improvements are commercial in nature); and

Remain in place for a period of time, usually two years or more, after the exchange concludes with rent flowing from tenant to landlord.Exchange commentators agree that these kinds of Related Party Leasehold Improvement Exchanges can be structured within the safe harbor, provided the Taxpayer acquires the leasehold interest plus improvements within 180 days of commencing the exchange. Several IRS private letter rulings also approve this structure including: LTR 201408019 (Feb. 21, 2014); LTR 200251008 (Dec. 20, 2002); and LTR 200329021 (Jul. 18, 2003).

Gain a better understanding of the process through this flyer, Leasehold Improvement Exchange.

What if the Same Taxpayer owns both the Relinquished and Replacement Properties?

As you likely surmised, the first step in this type of 1031 exchange is identifying the tax owner of the Relinquished Property and the Replacement Property.

If those two entities or individuals are the same Taxpayer, then it’s necessary to take sufficient advance planning steps to inject a Related Party into the proposed transaction. To successfully structure a Leasehold Improvement Exchange, there are several methods for incorporating a Related Party into the proposed transaction. I will outline one such technique below. However, before doing so, we must discuss some issues implicated under the 1031 Exchange regulations when proceeding with a Leasehold Improvement Exchange.

When the Same Taxpayer owns not only the land on which improvements are to be built, but also the Relinquished Property(ies), issues present such as the “exchange” requirement, which requires a reciprocal transfer of property between two separate parties. Also raised in these scenarios is the “like-kind” requirement. Navigating each of these elements is vital for a successful exchange and requires advance planning and an independent business purpose.

“Like-Kind” Requirement

As for the “like-kind” requirement, while the acquisition of the newly constructed improvements are acquired from the Accommodator (rather than the Taxpayer) and may otherwise satisfy the exchange requirement, the IRS takes the position that improvements to existing real property alone, absent the acquisition of an interest in the underlying land, is not “like-kind” to a fee simple interest in real property. For example, to satisfy the “like-kind” standard, the improvements must be tethered to a real property interest. To that point, the IRS has taken the position that the assignment of a lessee’s interest in a lease of greater than 30 years, including options, to an exchanging Taxpayer is “like-kind” to a fee simple interest. Rev. Rul. 68-394. W

An additional issue surfaces when the Same Taxpayer owns the Replacement Property within 180 days of the Accommodator carving out a newly created leasehold interest to begin the parking arrangement. In Rev. Proc. 2004-51, the IRS specifically modified Rev. Proc. 2000-37 and excluded from the safe harbor parking arrangements where the Same Taxpayer owns Replacement Property during the 180-day period ending on the date the Accommodator acquires an “interest” in that property. Under this rule, an “interest” in the property is arguably a newly created leasehold estate because that interest is conveyed to the Accommodator from the fee simple owner of the base property. This 180-day look-back period means that simply transferring land to a Related Party and immediately commencing a parking arrangement may not be a viable strategy.

Within Rev. Proc. 2004-51 the IRS and Treasury indicated they are:

“…continuing to study parking transactions, including transactions in which a person related to the taxpayer transfers a leasehold in land to an accommodation party and the accommodation party makes improvements to the land and transfers the leasehold with the improvements to the taxpayer in exchange for other real estate. Rev. Proc. 2004-51, 2004-2 CB 294 §2.06.”

So, although there may be an elevated risk of adverse exchange treatment where the Same Taxpayer owns Replacement Property per the rules and requirements outlined above, some possible resolutions exist. One such resolution is to have the Taxpayer contribute the Replacement base Property to a Related Party or different Taxpayer greater than 180 days prior to commencing the parking arrangement. After the lapse of 181 days, the Accommodator would then carve out a long-term leasehold (30 year or greater) directly with the Related Party and build out tenant improvements. Since the modification under Rev. Proc 2004-51 limits the look-back period to a definite time period (rather than disqualifying all property ever owned by a Taxpayer), it appears that if structured this way a subsequent Leasehold Improvement Exchange could be completed within the safe harbor.

“Independent Business Purpose” Requirement

An additional consideration when transferring the fee simple interest to a Related Party in advance of a Leasehold Improvement Exchange, is the independent business purpose requirement. Under this requirement, any transfer should be supported by an independent non-tax related business purpose. If no such independent business purpose exists for the transfer, then the theoretical risk is that the IRS would disregard the transfer and would still consider the Taxpayer to be the tax owner fee simple interest.

Some exchange commentators take the position an independent business purpose could perhaps be evidenced by: (1) additional liability protection as to a Taxpayer’s other assets; or (2) a need to establish a separate entity for holding only the fee simple interest in land as opposed to developing and leasing new improvements initiating a need for new management responsibilities. We defer to the Taxpayer’s advisors to determine whether there exists an independent business purpose for the change of ownership.

As discussed, this resolution is designed to preserve the “exchange” requirement, the “like-kind” requirement, the 180-day look-back under Rev. Proc. 2004-51, and to prevent “merger of title.” Merger of title is yet another factor in the analysis and occurs when the Accommodator steps out following construction and conveys a long-term leasehold interest and tenant improvements to the Taxpayer who finds themselves as both tenant (lessee) and landlord (lessor) under the lease agreement. In this scenario, by Operation of Law, merger of the leasehold interest with the fee simple interest occurs, thereby destroying the leasehold interest tethered to the improvements which is vital to preserve the like-kind requirement referenced above.

However, when a Related Party is involved as the landlord, then the title to the fee simple interest and long-term leasehold interest will not merge because there are separate and distinct tax owners on either side of the lease. In other words, the Taxpayer did not receive a non-permitted interest from a related party, rather he received the leasehold improvements solely from the EAT.

Example of a Leasehold Used in a 1031 Exchange

Mr. Rancher owns several properties in Southeast Colorado under his single-member LLC: SE Cattle Company, LLC. One such property is a debt free 80-acre tract of land with a calving barn for 200 head of cattle. Mr. Rancher is offered above market value for his 80-acre tract from a large retail distribution center. His temptation to capitalize on the offer is restrained by concern for high interest rates on new debt, low inventory, and above market asking prices on possible Replacement Property. As a result, he may not be able find a suitable Replacement Property should he accept the offer from the prospective buyer.

Nevertheless, Mr. Rancher’s daughter, a Related Party, owns a separate and distinct 150-acres of land in Colorado which needs substantial improvements for a newly anticipated horse arena, state-of-the-art calving barn, and fencing for up to 300 head of cattle.

Mr. Rancher’s local CPA recommends he contact a 1031 Exchange Qualified Intermediary well versed in ag-related property transactions to see if they have any ideas or solutions for his current dilemma.

Upon discussing his situation with one of Accruit’s staff attorneys, Mr. Rancher learns he can engage the services of Accruit as a Qualified Intermediary (“QI”) and as an Exchange Accommodation Titleholder (“EAT”), the latter of which is wholly owned by Accruit Exchange Accommodation Services, LLC, to facilitate a Leasehold Improvement Exchange. Mr. Rancher decides to initiate the proposed 1031 Exchange and accepts the $897,000.00 offer on his 80-acre tract. After closing costs, $871,000.00 in net exchange proceeds are held with the QI for the benefit of SE Cattle Company, LLC. Immediately thereafter, the EAT carves out and acquires a newly created long-term leasehold interest from Mr. Rancher’s daughter who serves as the lessor (i.e. landlord).

Through a Leasehold Improvement Exchange, SE Cattle Company, LLC, will authorize the QI to make progress payments to the EAT for constructing tenant improvements including a horse arena, state-of-the-art calving barn, and fencing for up to 300 head of cattle. The EAT then spends the $871,000.00 for construction costs within 180 days following the closing date of the 80-acre tract. Upon completion, the long-term leasehold interest and newly constructed tenant improvements are assigned by the EAT to SE Cattle Company, LLC, as like-kind Replacement Property prior to the 180th day following the closing on the Relinquished Property.

Mr. Rancher was able to utilize a long-term leasehold on property owned by a Related Party to complete a Leasehold Improvement Exchange and capitalize on all the benefits a 1031 Exchange has to offer, most notably deferring various level of tax including depreciation recapture, capital gains, applicable state taxes, and net investment income tax.

Summary

In conclusion, a Leasehold Improvement Exchange provides an opportunity to take advantage of the tax deferral benefits a 1031 Exchange offers when an investor holds multiple properties. An important takeaway is that proper planning and adequate lead time are required to ensure an exchange involving a long-term leasehold is structured properly.

The key is advance planning, and it is vital to have the experience of an Accruit subject-matter expert to structure a Leasehold Improvement Exchange. While it may seem overwhelming, these exchanges are common, and they provide the Taxpayer with great optionality, and can be completed within the safe harbor of Rev. Proc. 2000-37. Accruit staff attorneys have many other structuring possibilities that we can provide additional insight on for your consideration.

As always, we encourage property owners to invoke the advice of their attorneys, financial advisors, and CPA when considering any disposition of property.

The material in this blog is presented for informational purposes only. The information presented is not investment, legal, tax or compliance advice. Accruit performs the duties of a Qualified Intermediary, and as such does not offer or sell investments or provide investment, legal, or tax advice. -

How to Utilize a 1031 Exchange on Related Party or Same Taxpayer Property

With interest rates at a 15-year high and real estate values resisting a turn to the downside, purchasing Replacement Property, especially one that requires financing, isn’t as attractive as it was previously in lower interest rate market environments.

An alternative option for Taxpayers is exploring the possibility of a Leasehold Improvement Exchange, accommodated by an Accruit-owned entity, on a newly created long-term leasehold interest.

In 2000, the IRS issued Revenue Procedure 2000-37, which created a “safe harbor” for certain “parking” arrangements (i.e., where an accommodator temporarily holds title to exchange property), including Improvement Exchanges where a taxpayer desires to spend exchange value making improvements to Replacement Property.

A Leasehold Improvement Exchange is a variation of the kind of parking arrangement (i.e. reverse exchange) most used when a Related Party owns the base Replacement Property. Since, subject to limited exceptions outside the purview of this article, a Taxpayer cannot acquire a fee simple interest in real property from a Related Party.

In addition, although not a Leasehold Improvement issue, a Taxpayer cannot improve property once acquired by the Taxpayer, even if acquired from an unrelated party. The use of a parking arrangement is required if the Taxpayer plans to use exchange value to improve a real property interest.

This article outlines the planning, structuring, and regulation implicated when contemplating a Leasehold Improvement Exchange.

What is a Related Party to the Taxpayer?

The first step in structuring a Leasehold Improvement Exchange is understanding how the regulations define a Related Party. For purposes of § 1031(f), the term “related person” means any person bearing a relationship to the Taxpayer described in § 267(b) or 707(b)(1). The most common Related Parties implicated in a Leasehold Improvement Exchange are as follows:Members of the same family unit (siblings, spouse, ancestors, and lineal descendants);

Two partnerships in which the same person or persons own, directly or indirectly, more than a 50% capital interest or a 50% profits interest, in both partnerships;

A partnership and a person owning, directly or indirectly, more than a 50% capital interest or a 50% profits interest, in such partnership;

A corporation and a partnership if the same person or persons own: more than 50% in value of the outstanding stock of the corporation, and more than 50% of the capital interest, or the profits interest, in the partnership; and

Two corporations that are in the same controlled group.Read our extensive Related Party article for a more in-depth explanation of Related Party in relation to a 1031 Exchange.

Process of Leasehold Improvement Exchange

The structure of a Leasehold Improvement Exchange involves an Accommodator (as opposed to a Qualified Intermediary, which serves a different exchange function) carving out and acquiring a long-term interest in a ground lease from the fee simple owner of the land (i.e. the Related Party). The Accommodator would be a newly created Accruit-owned special purpose limited liability company specific for the transaction. The Accommodator uses the exchange value to pay construction and material invoices and incorporate specified tenant improvements on the ground lease. The source of Accommodator financing to pay for these costs may originate from exchange funds, bridge financing, and/or cash from the taxpayer.

The lease from the Related Party as lessor to the Accommodator as lessee must be a fair market lease supported by fair market rent to be paid by the lessee to the ground lessor. Under the safe harbor of the Reverse Exchange regulations promulgated in Rev. Proc. 2000-37, the rent expense can be lent from the Taxpayer to the Accommodator.

At the conclusion, after the necessary exchange value is injected into tenant improvements or prior to the 180th day, whichever occurs first, the Taxpayer acquires the interest in the long-term lease and newly constructed improvements from the Accommodator using funds generated from the sale of the Relinquished Property. Any applicable bridge loans are paid down or satisfied using these funds. As a result, the Replacement Property is the: (1) improvements acquired from the Accommodator; and (2) the long-term leasehold interest. Of note, the Taxpayer will only be able to acquire and receive credit for the tenant improvements, materials, and workmanship which are vertical and incorporated into the leasehold estate prior to the 180th day, but will not be able to allocate exchange value to those materials still on the worksite nor pre-pay the contractor.

Upon conveyance from the Accommodator to the Taxpayer, the leasehold interest and term must:Have 30 years or more remaining on the term upon transfer to the Taxpayer as Replacement Property (or 39 years if the replacement property improvements are commercial in nature); and

Remain in place for a period of time, usually two years or more, after the exchange concludes with rent flowing from tenant to landlord.Exchange commentators agree that these kinds of Related Party Leasehold Improvement Exchanges can be structured within the safe harbor, provided the Taxpayer acquires the leasehold interest plus improvements within 180 days of commencing the exchange. Several IRS private letter rulings also approve this structure including: LTR 201408019 (Feb. 21, 2014); LTR 200251008 (Dec. 20, 2002); and LTR 200329021 (Jul. 18, 2003).

Gain a better understanding of the process through this flyer, Leasehold Improvement Exchange.

What if the Same Taxpayer owns both the Relinquished and Replacement Properties?

As you likely surmised, the first step in this type of 1031 exchange is identifying the tax owner of the Relinquished Property and the Replacement Property.

If those two entities or individuals are the same Taxpayer, then it’s necessary to take sufficient advance planning steps to inject a Related Party into the proposed transaction. To successfully structure a Leasehold Improvement Exchange, there are several methods for incorporating a Related Party into the proposed transaction. I will outline one such technique below. However, before doing so, we must discuss some issues implicated under the 1031 Exchange regulations when proceeding with a Leasehold Improvement Exchange.

When the Same Taxpayer owns not only the land on which improvements are to be built, but also the Relinquished Property(ies), issues present such as the “exchange” requirement, which requires a reciprocal transfer of property between two separate parties. Also raised in these scenarios is the “like-kind” requirement. Navigating each of these elements is vital for a successful exchange and requires advance planning and an independent business purpose.

“Like-Kind” Requirement

As for the “like-kind” requirement, while the acquisition of the newly constructed improvements are acquired from the Accommodator (rather than the Taxpayer) and may otherwise satisfy the exchange requirement, the IRS takes the position that improvements to existing real property alone, absent the acquisition of an interest in the underlying land, is not “like-kind” to a fee simple interest in real property. For example, to satisfy the “like-kind” standard, the improvements must be tethered to a real property interest. To that point, the IRS has taken the position that the assignment of a lessee’s interest in a lease of greater than 30 years, including options, to an exchanging Taxpayer is “like-kind” to a fee simple interest. Rev. Rul. 68-394. W

An additional issue surfaces when the Same Taxpayer owns the Replacement Property within 180 days of the Accommodator carving out a newly created leasehold interest to begin the parking arrangement. In Rev. Proc. 2004-51, the IRS specifically modified Rev. Proc. 2000-37 and excluded from the safe harbor parking arrangements where the Same Taxpayer owns Replacement Property during the 180-day period ending on the date the Accommodator acquires an “interest” in that property. Under this rule, an “interest” in the property is arguably a newly created leasehold estate because that interest is conveyed to the Accommodator from the fee simple owner of the base property. This 180-day look-back period means that simply transferring land to a Related Party and immediately commencing a parking arrangement may not be a viable strategy.

Within Rev. Proc. 2004-51 the IRS and Treasury indicated they are:

“…continuing to study parking transactions, including transactions in which a person related to the taxpayer transfers a leasehold in land to an accommodation party and the accommodation party makes improvements to the land and transfers the leasehold with the improvements to the taxpayer in exchange for other real estate. Rev. Proc. 2004-51, 2004-2 CB 294 §2.06.”

So, although there may be an elevated risk of adverse exchange treatment where the Same Taxpayer owns Replacement Property per the rules and requirements outlined above, some possible resolutions exist. One such resolution is to have the Taxpayer contribute the Replacement base Property to a Related Party or different Taxpayer greater than 180 days prior to commencing the parking arrangement. After the lapse of 181 days, the Accommodator would then carve out a long-term leasehold (30 year or greater) directly with the Related Party and build out tenant improvements. Since the modification under Rev. Proc 2004-51 limits the look-back period to a definite time period (rather than disqualifying all property ever owned by a Taxpayer), it appears that if structured this way a subsequent Leasehold Improvement Exchange could be completed within the safe harbor.

“Independent Business Purpose” Requirement

An additional consideration when transferring the fee simple interest to a Related Party in advance of a Leasehold Improvement Exchange, is the independent business purpose requirement. Under this requirement, any transfer should be supported by an independent non-tax related business purpose. If no such independent business purpose exists for the transfer, then the theoretical risk is that the IRS would disregard the transfer and would still consider the Taxpayer to be the tax owner fee simple interest.

Some exchange commentators take the position an independent business purpose could perhaps be evidenced by: (1) additional liability protection as to a Taxpayer’s other assets; or (2) a need to establish a separate entity for holding only the fee simple interest in land as opposed to developing and leasing new improvements initiating a need for new management responsibilities. We defer to the Taxpayer’s advisors to determine whether there exists an independent business purpose for the change of ownership.

As discussed, this resolution is designed to preserve the “exchange” requirement, the “like-kind” requirement, the 180-day look-back under Rev. Proc. 2004-51, and to prevent “merger of title.” Merger of title is yet another factor in the analysis and occurs when the Accommodator steps out following construction and conveys a long-term leasehold interest and tenant improvements to the Taxpayer who finds themselves as both tenant (lessee) and landlord (lessor) under the lease agreement. In this scenario, by Operation of Law, merger of the leasehold interest with the fee simple interest occurs, thereby destroying the leasehold interest tethered to the improvements which is vital to preserve the like-kind requirement referenced above.

However, when a Related Party is involved as the landlord, then the title to the fee simple interest and long-term leasehold interest will not merge because there are separate and distinct tax owners on either side of the lease. In other words, the Taxpayer did not receive a non-permitted interest from a related party, rather he received the leasehold improvements solely from the EAT.

Example of a Leasehold Used in a 1031 Exchange

Mr. Rancher owns several properties in Southeast Colorado under his single-member LLC: SE Cattle Company, LLC. One such property is a debt free 80-acre tract of land with a calving barn for 200 head of cattle. Mr. Rancher is offered above market value for his 80-acre tract from a large retail distribution center. His temptation to capitalize on the offer is restrained by concern for high interest rates on new debt, low inventory, and above market asking prices on possible Replacement Property. As a result, he may not be able find a suitable Replacement Property should he accept the offer from the prospective buyer.

Nevertheless, Mr. Rancher’s daughter, a Related Party, owns a separate and distinct 150-acres of land in Colorado which needs substantial improvements for a newly anticipated horse arena, state-of-the-art calving barn, and fencing for up to 300 head of cattle.

Mr. Rancher’s local CPA recommends he contact a 1031 Exchange Qualified Intermediary well versed in ag-related property transactions to see if they have any ideas or solutions for his current dilemma.

Upon discussing his situation with one of Accruit’s staff attorneys, Mr. Rancher learns he can engage the services of Accruit as a Qualified Intermediary (“QI”) and as an Exchange Accommodation Titleholder (“EAT”), the latter of which is wholly owned by Accruit Exchange Accommodation Services, LLC, to facilitate a Leasehold Improvement Exchange. Mr. Rancher decides to initiate the proposed 1031 Exchange and accepts the $897,000.00 offer on his 80-acre tract. After closing costs, $871,000.00 in net exchange proceeds are held with the QI for the benefit of SE Cattle Company, LLC. Immediately thereafter, the EAT carves out and acquires a newly created long-term leasehold interest from Mr. Rancher’s daughter who serves as the lessor (i.e. landlord).

Through a Leasehold Improvement Exchange, SE Cattle Company, LLC, will authorize the QI to make progress payments to the EAT for constructing tenant improvements including a horse arena, state-of-the-art calving barn, and fencing for up to 300 head of cattle. The EAT then spends the $871,000.00 for construction costs within 180 days following the closing date of the 80-acre tract. Upon completion, the long-term leasehold interest and newly constructed tenant improvements are assigned by the EAT to SE Cattle Company, LLC, as like-kind Replacement Property prior to the 180th day following the closing on the Relinquished Property.

Mr. Rancher was able to utilize a long-term leasehold on property owned by a Related Party to complete a Leasehold Improvement Exchange and capitalize on all the benefits a 1031 Exchange has to offer, most notably deferring various level of tax including depreciation recapture, capital gains, applicable state taxes, and net investment income tax.

Summary

In conclusion, a Leasehold Improvement Exchange provides an opportunity to take advantage of the tax deferral benefits a 1031 Exchange offers when an investor holds multiple properties. An important takeaway is that proper planning and adequate lead time are required to ensure an exchange involving a long-term leasehold is structured properly.

The key is advance planning, and it is vital to have the experience of an Accruit subject-matter expert to structure a Leasehold Improvement Exchange. While it may seem overwhelming, these exchanges are common, and they provide the Taxpayer with great optionality, and can be completed within the safe harbor of Rev. Proc. 2000-37. Accruit staff attorneys have many other structuring possibilities that we can provide additional insight on for your consideration.

As always, we encourage property owners to invoke the advice of their attorneys, financial advisors, and CPA when considering any disposition of property.

The material in this blog is presented for informational purposes only. The information presented is not investment, legal, tax or compliance advice. Accruit performs the duties of a Qualified Intermediary, and as such does not offer or sell investments or provide investment, legal, or tax advice. -

The Compounding Benefits of a 1031 Exchange

While financial benefits of a 1031 Exchange are experienced within the 180-day exchange period, there are additional, compounding benefits that are not readily visible at the completion of your exchange.

Let’s take a look at the long-term benefits of utilizing a 1031 Exchange for your qualifying real estate transaction.

Suzy Investor owns a retail center she has been renting out over the past 20 years. She has taken annual depreciation deductions of $10,256 since 1990, reducing her tax basis to $244,880. She decides to sell the retail center at market value of $1,250,000, and rid herself of management responsibility by reinvesting into a passive investment opportunity, such as a DST.

Without leveraging a 1031 Exchange, Suzy will incur the following tax liability, leaving her only $942,400 to reinvest.

federal capital gains tax (20%): $153,000

depreciation recapture tax (25%): $51,280

state capital gains (5% varies by state): $38,250

net investment income tax (3.8%): $29,070

Total Tax Liability: $271,600

Reinvestment Total Without a 1031 exchange: $942,400 ($1,250,000 – $271,600)

However, should Suzy engage a Qualified Intermediary prior to the sale of her retail center and structure her transaction as a 1031 Exchange, she will defer all levels of tax above and have the total $1.25 Million to reinvest.

The immediate benefit is obvious; Suzy has an additional $271,600 to reinvest. The less obvious benefit is how that additional amount compounds over the proceeding years. With Suzy utilizing a 1031 Exchange and reinvesting the full $1.25 million, at a 7% compounded rate of return over the next 10 years she will have earned nearly double the investment for a total of $2.45 Million.

Without a 1031 Exchange, the reinvestment amount of just $942,400 after 10 years at the same compounding rate of return, only earns $1.85 Million, roughly only $500,000 more than her original reinvestment amount with the use of a 1031 Exchange. That equates to $600,000 less over 10 years should a 1031 Exchange not be utilized.

Utilizing a 1031 Exchange not only provides investors with immediate benefits, it continues to produce returns on investment in the future.

The material in this blog is presented for informational purposes only. The information presented is not investment, legal, tax or compliance advice. Accruit performs the duties of a Qualified Intermediary, and as such does not offer or sell investments or provide investment, legal, or tax advice. -

The Compounding Benefits of a 1031 Exchange

While financial benefits of a 1031 Exchange are experienced within the 180-day exchange period, there are additional, compounding benefits that are not readily visible at the completion of your exchange.

Let’s take a look at the long-term benefits of utilizing a 1031 Exchange for your qualifying real estate transaction.

Suzy Investor owns a retail center she has been renting out over the past 20 years. She has taken annual depreciation deductions of $10,256 since 1990, reducing her tax basis to $244,880. She decides to sell the retail center at market value of $1,250,000, and rid herself of management responsibility by reinvesting into a passive investment opportunity, such as a DST.

Without leveraging a 1031 Exchange, Suzy will incur the following tax liability, leaving her only $942,400 to reinvest.

federal capital gains tax (20%): $153,000

depreciation recapture tax (25%): $51,280

state capital gains (5% varies by state): $38,250

net investment income tax (3.8%): $29,070

Total Tax Liability: $271,600

Reinvestment Total Without a 1031 exchange: $942,400 ($1,250,000 – $271,600)

However, should Suzy engage a Qualified Intermediary prior to the sale of her retail center and structure her transaction as a 1031 Exchange, she will defer all levels of tax above and have the total $1.25 Million to reinvest.

The immediate benefit is obvious; Suzy has an additional $271,600 to reinvest. The less obvious benefit is how that additional amount compounds over the proceeding years. With Suzy utilizing a 1031 Exchange and reinvesting the full $1.25 million, at a 7% compounded rate of return over the next 10 years she will have earned nearly double the investment for a total of $2.45 Million.

Without a 1031 Exchange, the reinvestment amount of just $942,400 after 10 years at the same compounding rate of return, only earns $1.85 Million, roughly only $500,000 more than her original reinvestment amount with the use of a 1031 Exchange. That equates to $600,000 less over 10 years should a 1031 Exchange not be utilized.

Utilizing a 1031 Exchange not only provides investors with immediate benefits, it continues to produce returns on investment in the future.

The material in this blog is presented for informational purposes only. The information presented is not investment, legal, tax or compliance advice. Accruit performs the duties of a Qualified Intermediary, and as such does not offer or sell investments or provide investment, legal, or tax advice.